Being a value investor in 2020 has felt like being a polar bear in Arizona during the summer heat. With that said, we are in the business of buying securities at deep discounts to intrinsic value. Over time, that has worked out extremely well, and frankly, I believe we are close to an inflection point. Bank of America (BAC) is one of the strongest franchises in any industry in the United States. The company has been transformed into a much more conservative and financially sound bank that is proving its mettle despite enduring the worst economic quarter since the Great Depression. Bank of America is deeply undervalued and likely to be a big winner over the next 3-5 years.

Brian Moynihan, the CEO of Bank of America, is one of the most underrated executives in America. He is not necessarily as eloquent as Jamie Dimon or James Gorman can be, but he is extremely effective and disciplined. Bank of America going into the Financial Crisis was not as bad as history makes it out to be. What killed it were the acquisitions of Countrywide Financial and the price it paid for Merrill Lynch. Countrywide caused tens of billions of losses and litigation. Merrill Lynch was a great strategic fit, but realistically, it could have likely been purchased for half the price or less a week later, given what was going on back then. BAC did have too much unsecured credit exposure, which caused huge losses during the Great Recession, which is night and day from where the company sits today.

Since Moynihan took over, he has created a much more durable and conservative franchise. The trading business is flow-driven; it is not making the outsized bets of a Goldman Sachs (GS), but it is capital efficient and allows the bank to take advantage of fortuitous environments like we saw in Q2 for trading. Today, the unsecured card portfolio is roughly half of what it was going into the Great Recession and with better asset quality. The commercial real estate portfolio has considerably less exposure to construction loans, which can be very troublesome in times of economic turmoil. The company has really improved as an underwriter.

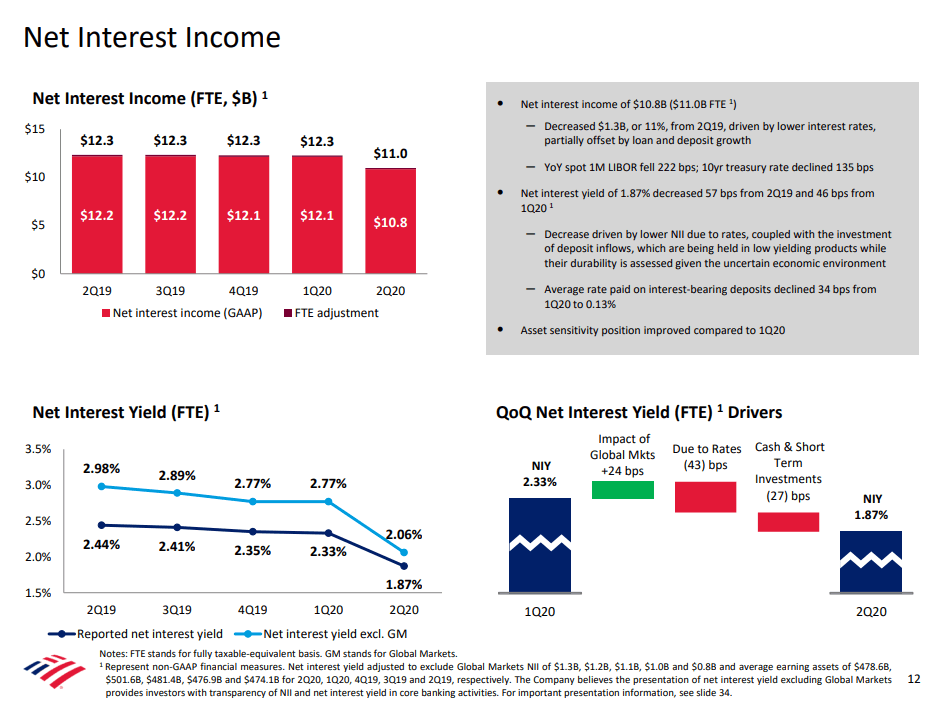

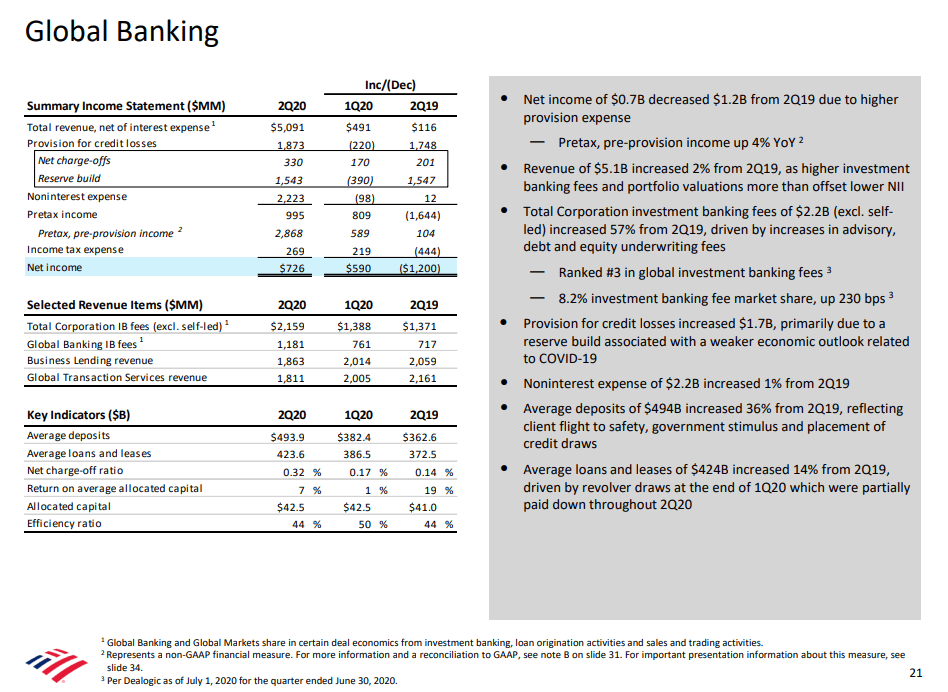

On July 16th, Bank of America reported an impressive 2nd quarter, given the challenging backdrop of COVID-19 and the associated lockdown. Total revenue of $22.3 billion was down 3% YoY, largely due to lower interest rates. The provision for credit losses was a sizable $5.1 billion, up $4.3 billion from a year ago and was up $.9 billion from the 1st quarter. Non-interest expense was up $.1 billion, due to COVID-19 costs such as additional cleaning, etc. Pretax income of $3.8 billion was down 58% YoY, largely due to the credit reserve build. Pretax, pre-provision income of $8.9 billion, was only down 9% YoY, largely due to lower rates. Net income of $3.5 billion was down 52% YoY, while diluted EPS of $.37 was down 50%. In what was undeniably a trough quarter, BAC posted a ROE of 5.4%, and a ROTCE of 7.6%.

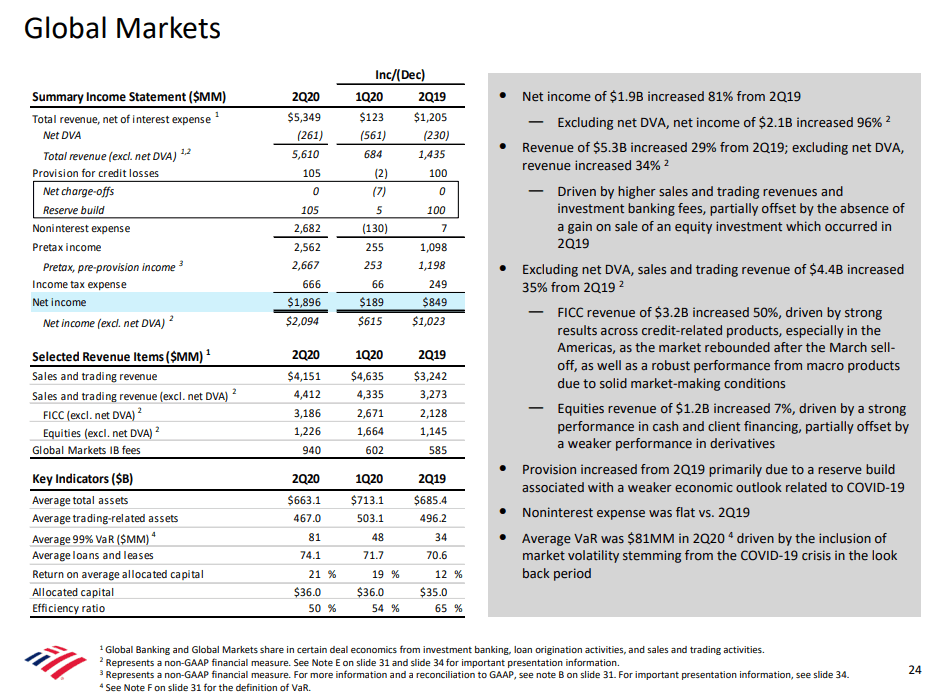

Global Markets performed very well with sales and trading revenue excluding DVA of $4.4 billion, which was up 35% YoY. Investment banking fees of $2.2 billion were a record and grew 57% YoY. Overall, the company saw a $1.9 billion improvement in sales, trading, and investment banking YoY. The unit produced $1.9 billion in after-tax profit. I have been writing research reports on banks and investing in them for a long time, and this is likely not my first or last criticism of the analysts that cover them. I have seen critiques about how other banks outperformed BAC during the 2nd quarter, but all the banks have different mixes and risk appetites. Bank of America is not a swashbuckling trading company. It is a flow-driven business with excellent wealth management/investment banking capabilities. The difference is it has as good of a retail and business banking franchise as exists in this country, along with JPMorgan (JPM). The myopic focus on any one quarter, or one metric such as net interest margins, are just a few areas where the analyst community falls short.

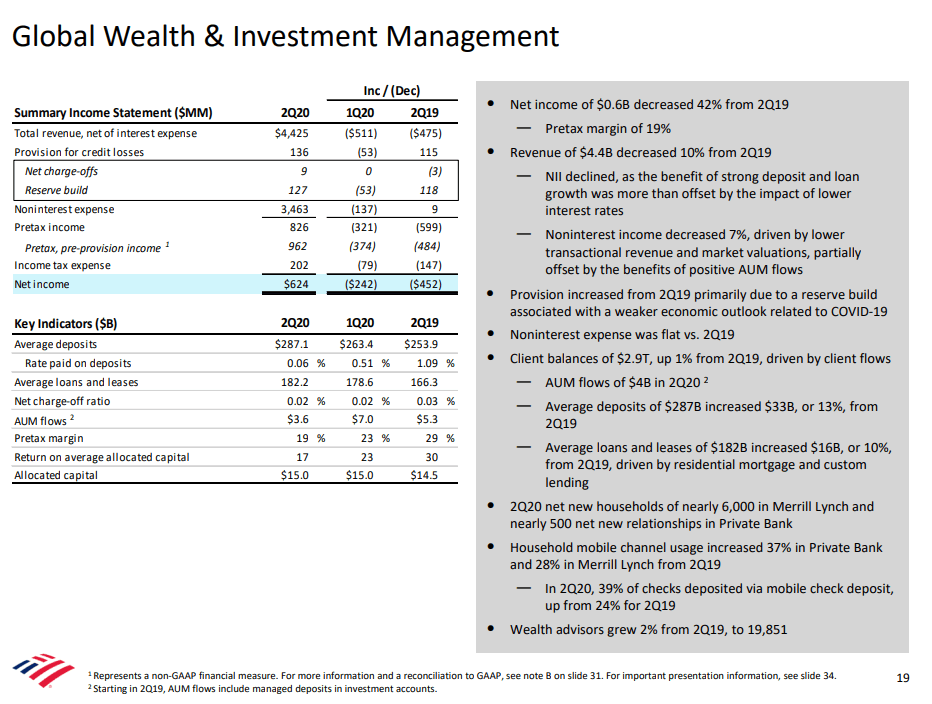

Merrill Lynch performed adequately in the quarter, generating net income of $624 million, which was down 42% YoY, driven by a 10% decline in revenue, as well as a higher provision expense. Total client balances rose to $2.9 trillion after a rebound in the equity markets. Merrill Lynch and the Private Bank continue to gain clients, despite a tough environment. The Wealth Management business is a true gem for BAC and would likely trade at steep premium to book value if ever spun-out, although I do not see that happening. Fee revenue that does not tie up the balance sheet is a huge benefit for the bank. The earnings trajectory should go up as they are likely to see less credit losses, and the revenue will reflect higher market levels.

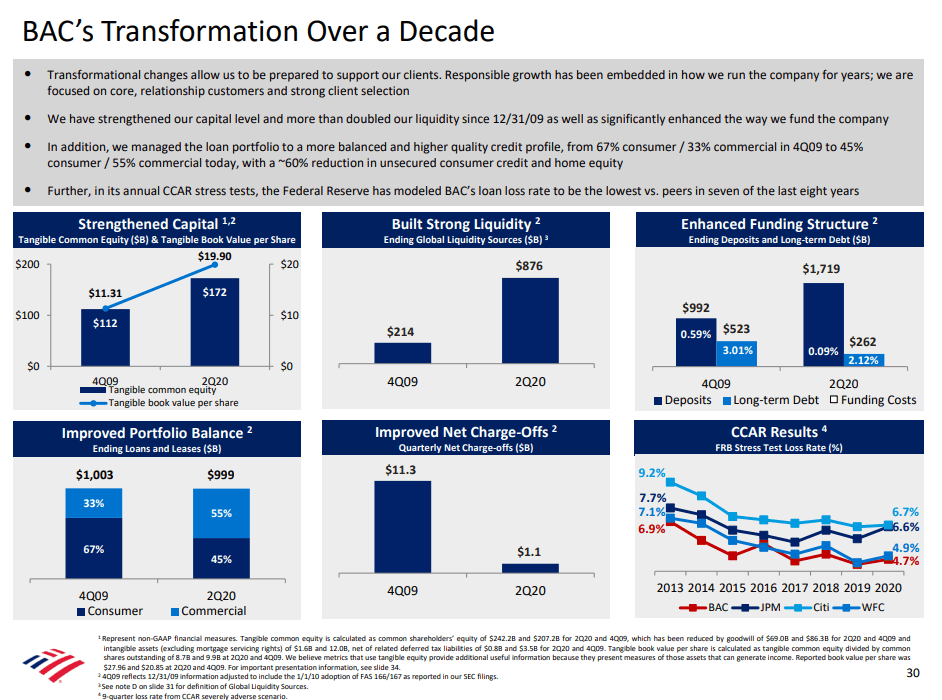

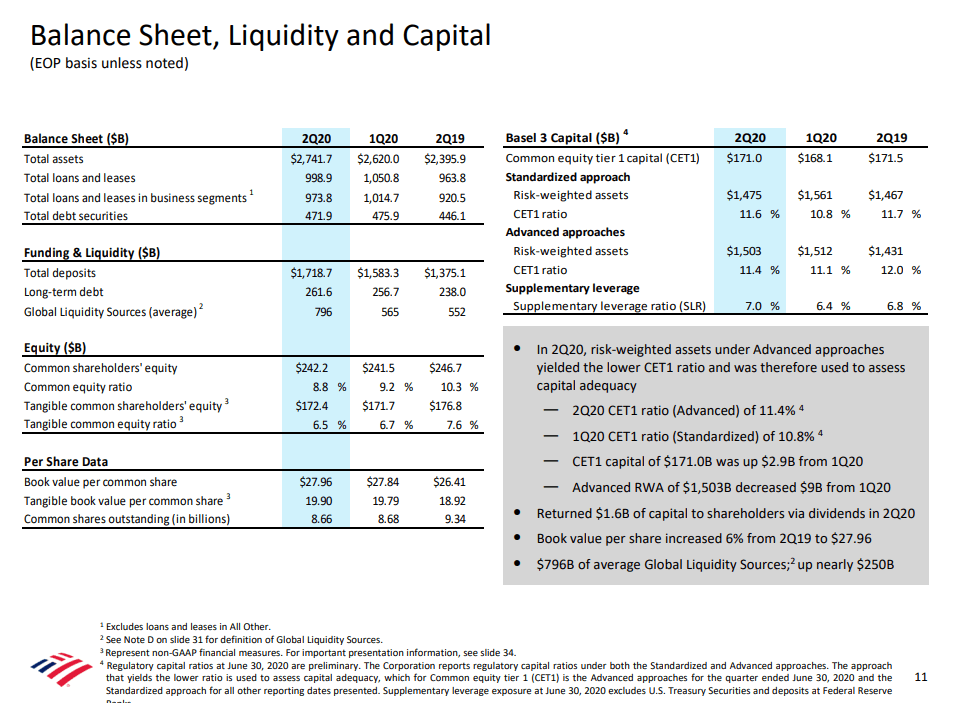

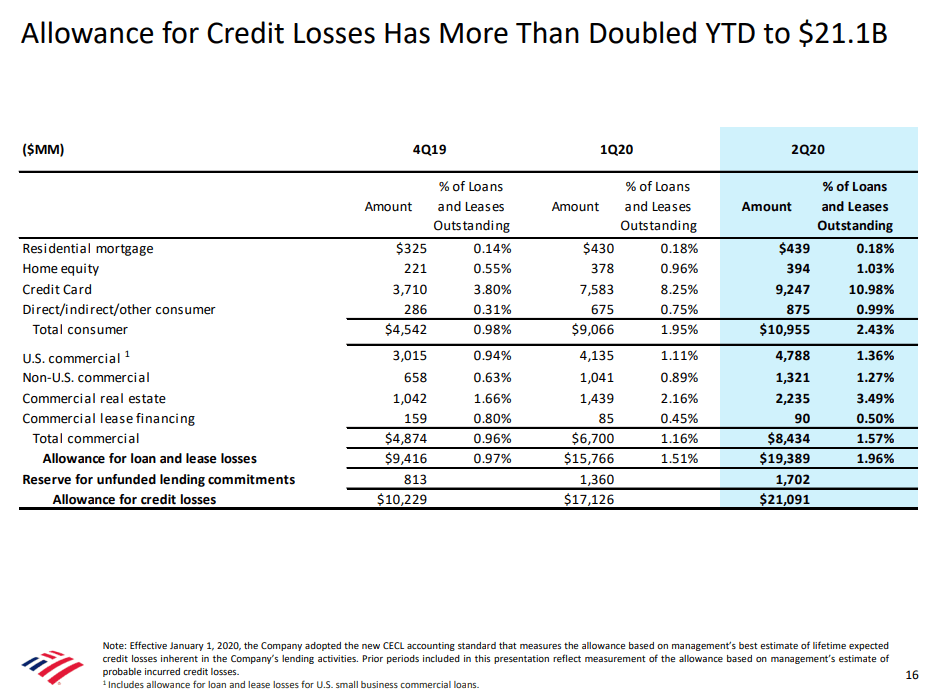

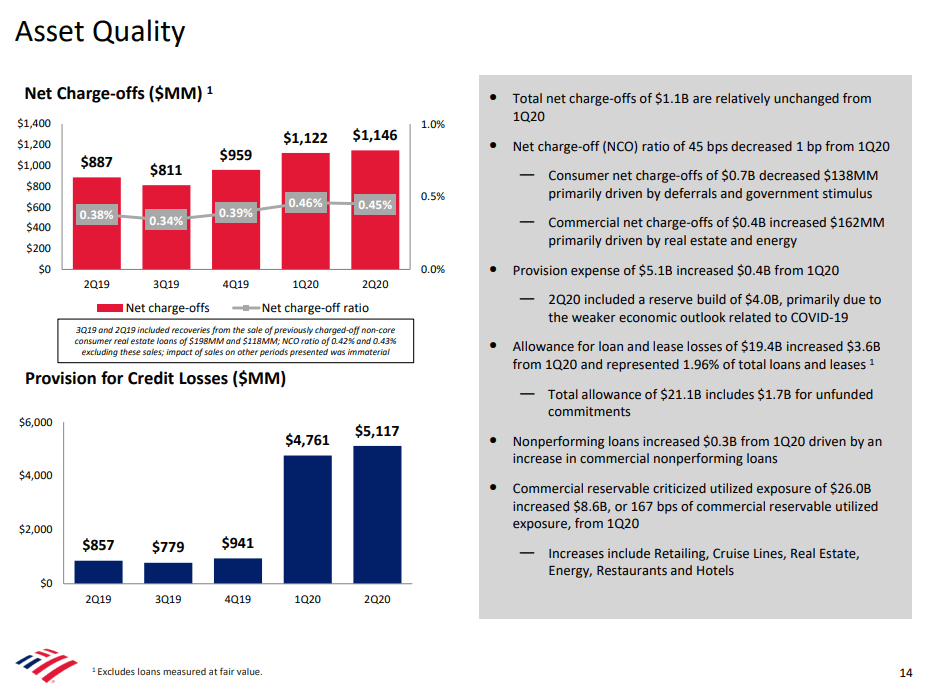

BAC saw growth in both book value per share and tangible book value per share in the quarter to $27.96 and $19.90, respectively. The CET1 ratio improved to 11.6% from 10.8% in the 1st quarter. The SLR stood at 7%, up from 6.4% in Q1. The bank has an astounding $796 billion of average Global Liquidity Source, up nearly $250 billion. Credit reserves have doubled since year-end to $21.1 billion. One of the scariest credit areas in the recession is commercial real estate, where BAC has $2.235 billion reserved for losses or 3.49% to CRE loans. Even if they doubled that, we are only talking about another $2.235 billion, for a company that earns roughly $9 billion in pretax pre-provision. The company has earned $7.5 billion through the 1st half of 2020, despite front-loading those loan losses to meet the new CECL requirements, which require banks to set aside all future loan losses on existing business upfront. Charge-offs were stable in the quarter at 45 basis points and non-performing loans only increased slightly. Obviously, future losses will be determined by the economy, employment, and likely federal stimulus measures.

BAC’s current operating assumptions for making credit projections are that unemployment ends this year around 10%, remains at 9% through the 1st half of 2021, and 7.5% at the end of 2021. That seems reasonable to me, and while of course, things could end up a bit worse, they also could end up a lot better. Delinquencies are not even close to what would be expected in an 11% unemployment scenario largely due to the unprecedented fiscal stimulus, so clearly the next fiscal package and ensuing employment reports will be important. I would not be surprised at all if the banks ultimately find themselves overly reserved, like they did during the Global Financial Crisis, which would mean future quarters see loan loss releases. I would not expect that until this drama is over and done, but BAC is standing in a great position and I am confident we have seen the worst of loan loss provisioning these past two quarters.

COVID-19 and the dreaded lockdown caused immense economic damage and shock, which the banks did everything they could do to help by providing forbearance and limiting certain fees. On credit cards, 85% of the deferrals were initiated in late March, early April, but has died down significantly. 95% that initiated were current on their payments when the deferral was requested, and more than 60% of the active deferrals have made at least one payment since going on deferral. 1/3rd have made payments every single month. Small business is clearly where the most pain is being felt and it is no surprise with the arbitrary lockdown policies, where a business can be forced to close without any notice whatsoever, even after spending tens of thousands to meet updated compliance regulations. Bank of America flagged in the 1st quarter that many of its requests came from doctors and dentists, who are mostly now able to operate, and according to an internal survey, 90% informed the bank they will not need to continue with the deferral.

Wells Fargo (WFC) is kind of where Bank of America was when Moynihan took over. Moynihan cut costs to a level in which many skeptics thought would be impossible, which continues to bear fruit today. Quarterly expenses were $13.4 billion, right in line with the 4-year range of between $13 and 13.5 billion, despite heavy investment in digitization. In that $13.4 billion, there was roughly $400 million of net impact of expenses and savings related to COVID-19.

At a recent price of $23.22, Bank of America offers a 3.02% dividend yield and trades at only 83% of book value per share. The market cap is $201 billion, and we get a business that has generated over $27 billion in net income in each of the last two years. Interest rates are very low, so the current earnings power is probably around $2.50 per share, but the potential for earnings growth is tremendous on any normalization on that front, let alone if reserves prove to be too aggressive. In a market where valuations are stretched, even a 10% earnings yield for this quality of a business seems too high. In summary, I love the stock here and think it should return 50% within 2-3 years.

Disclosure: I am/we are long BAC. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.