Gold has finally caught the wave of rising momentum that has lately propelled other commodities higher. A strengthening currency component is a major reason for this development, although there are other reasons for being bullish on gold in the months ahead. In this report, we’ll examine the growing weight of technical and fundamental evidence which supports higher gold prices in the early part of 2020.

Gold is poised to finish the final month of 2019 with its first notable gain since early September. It has also risen some 18% year to date and is on track to post its best year in nearly a decade. That in itself is a noteworthy accomplishment considering the significant pressure the metal faced for much of the fourth quarter.

Indeed, gold prices are finally showing signs of life after spending months in a downward-sloping trading range. U.S. political uncertainty has helped reverse somewhat gold’s flagging “fear factor” and has arguably increased safety-related demand for the metal in recent weeks. Yet there are other factors behind gold’s latest rebound which are far more worthy of our attention.

Let’s start by looking at the investor sentiment backdrop for the precious metal. After gold’s last major price peak nearly four months ago, the intense fears that investors experienced over the U.S.-Sino trade war earlier in the year have diminished. As uncertainty has evaporated, it has been replaced with a greater tolerance for risk as gold and other safe havens have been shunned in favor of equities. But while equities continue to enjoy favor among investors, gold has made a long-awaited comeback, and not because fear has returned with a vengeance. Rather, the recent drop of the U.S. dollar index has served as a catalyst for what should be a sustained rally in the coming months.

The weaker dollar in turn can be attributed to the increased optimism for a lasting solution to the trade dispute between China and the U.S. During the first nine months of 2019, the U.S. dollar index (DXY) was in the ascendant as trade-related uncertainties mounted. Trade war fears finally reached a crescendo in the late summer months before investors realized there was a legitimate chance of a mutually beneficial solution to the trade dispute being reached. When both nations agreed to roll back tariffs, investors celebrated by exiting the safety of the U.S. dollar and moving into industrial commodities which would benefit from renewed vigor among industry-dependent emerging nations.

One of the best illustrations of the flight from the dollar is the Invesco DB USD Bullish ETF (UUP), shown below. This dollar-tracking vehicle shows the extent to which the greenback has faltered lately under the return of investor optimism over the global economic outlook. With the trade outlook much improved, investors now have more reasons for buying commodities – including gold and other metals – in anticipation of a global manufacturing revival.

Source:

Source:

Gold’s fortunes are also closely tied with those of China and other emerging markets to some degree. Any decline in the U.S. dollar’s value is bound to boost the buying interest in the metal among consumers of nations like China and India due to the higher historical demand for gold as a personal savings and investment medium. As I previously pointed out, the relationship between a rising gold price and bullish emerging market stocks can be seen in the following chart. This chart compares the gold price with the iShares MSCI Emerging Markets ETF (EEM).

Source:

Source:

Now that the global trade outlook has substantially improved, the emerging markets ETF is showing more sustained strength than it has in several months. This is yet another piece of anecdotal evidence that supports a bullish intermediate-term gold outlook. See the 6-month performance of EEM shown below for a closer look at the gains made by emerging market equities.

Source:

Source:

There are other variables which support a bullish intermediate-term (3-6 month) outlook on the yellow metal, as well. One we’ve discussed already in a recent report is the powerful relative strength reflected in the following graph for the continuous contract palladium futures price. Palladium has been on a rip-and-tear in recent months, consistently powering to new highs even as the gold price languishes in a trading range. The most recent high in palladium was made just a couple of weeks ago, as can be seen below.

Source:

Source:

Not only has palladium historically served as a type of secondary hedging asset during times of geopolitical tensions, it’s also an important industrial metal whose usage is heavily predicated on a bullish global economic outlook. That palladium and other industrial metals have rallied as strongly as they have in recent months suggests that informed buyers anticipate increased usage of the metals in the intermediate-term outlook.

Another variable which is helping to support gold right now is the fact that Federal Reserve policymakers recently upheld the central bank’s stance on leaving interest rates unchanged at the latest FOMC meeting. This indicates that the bar to both cutting and raising rates remains high. The lower Fed funds rate in turn reduces the opportunity cost of holding bullion and also typically puts downward pressure on the dollar. Both factors bode well for gold’s intermediate-term outlook.

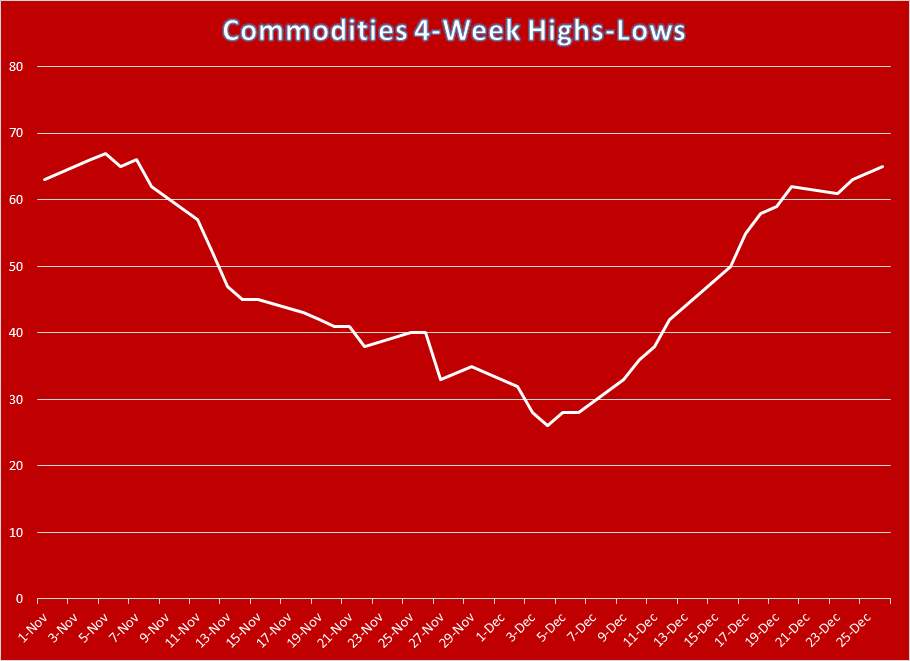

Yet another consideration for gold’s near-term outlook is the possibility that the internal momentum that is presently lifting many other commodity prices – including palladium – is beginning to spill over into the gold arena. Below is my favorite measure for the near-term incremental demand for the broad commodities market. It’s a 4-week rate of change indicator based on the new highs and lows for approximately 30 actively traded U.S. (non-financial) commodity futures.

Source:

As you can see, this indicator continues to rise which indicates that the near-term path of least resistance for the broad natural resource market is currently up. The upward push of this momentum wave of the last several weeks is finally spilling over into gold – just as it previously did for the palladium market.

Now that gold is experiencing some much-needed price momentum, gold bulls should be able to succeed in pushing the yellow metal back up to its Sept. 4 high of $1,566. The latest breakdown in the dollar index should make it very easy for the bulls to completely regain control over gold’s intermediate trend, along with the other factors mentioned here. The most important thing from a technical perspective is that gold remains above its widely watched (and psychologically significant) 50-day moving average on a weekly closing basis. That particular trendline can be seen at about the $1,485 level in the daily chart shown below.

Source:

In conclusion, investors have every reason to remain upbeat about the prospects for higher gold prices entering 2020. Although gold’s “fear factor” as it pertains to the U.S.-China trade war has diminished, the overall demand for the metal should grow based upon the improved manufacturing and trade outlook in gold-consuming nations like China and other emerging nations. In view of the factors discussed here, investors are therefore justified in maintaining longer-term holdings of the metal.

On a strategic note, I’m currently long the VanEck Vectors Gold Miners ETF (GDX) after its recent move above the $28.00 level. As discussed in previous writings, a move above $28.00 would strongly suggest that the bulls are making a serious “run on the stops” placed by the bears, who in turn would likely be forced into short-covering based on the tendency for round numbers to serve as a stop-loss magnet. That outlook appears to be justified based on the sharp nature of the recent rally in GDX. I’m using a level slightly under $27.13 (the Dec. 20 closing level) as the initial stop-loss for this trade on an intraday basis.

Disclosure: I am/we are long GDX. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.