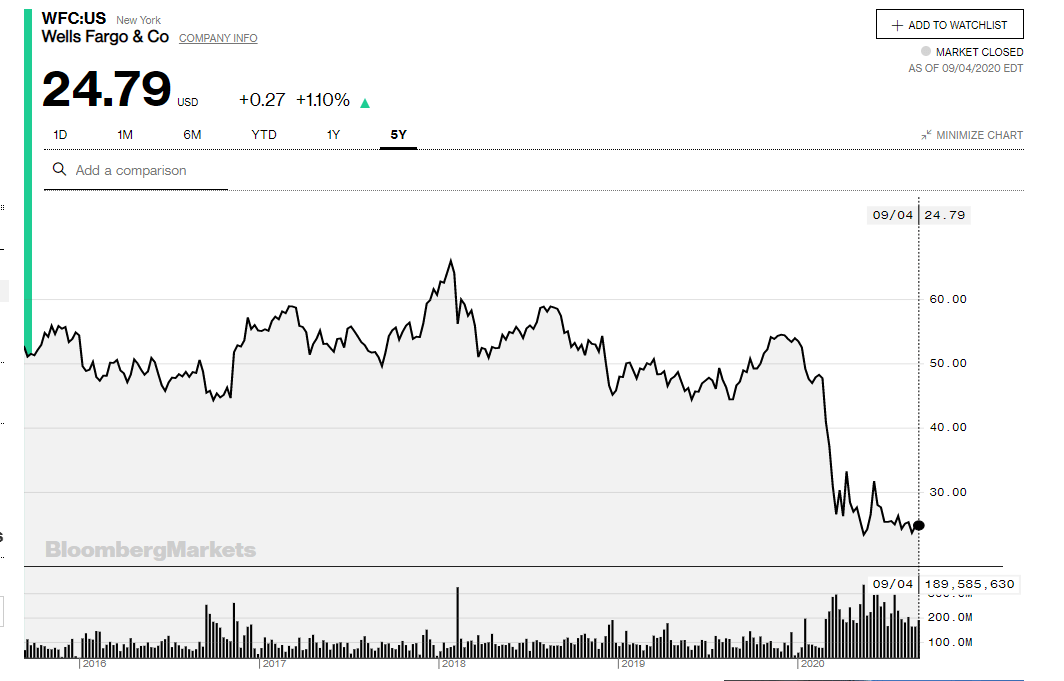

Berkshire Hathaway (NYSE:BRK.A) (NYSE:BRK.B) made a regulatory filing yesterday, disclosing that it has sold a further 100m shares in Wells Fargo (NYSE:WFC). Moves by Berkshire and Warren Buffett are closely followed on Seeking Alpha, reflecting Mr Buffett’s extraordinary track record over the long term. This does not mean you should copy Warren Buffett. Investors have to find their own way of doing things.

His recent moves in Wells Fargo are particularly questionable, given how far the stock has fallen from its peak.

Source: Bloomberg

First, put the move in context. Mr. Buffett has reduced his overall bank exposure, including various names outside WFC as well, which makes sound fundamental sense. The bank sector faces two broad and large uncertainties. One is the level of credit distress the Covid-19 lockdown economy will inflict. The other is the outlook for interest rates.

Here, the Fed’s recent guidance that it will let inflation run hot in order to support its employment mandate emphasised that we have a long way to go before the market will assume markedly higher rates “out there.”

The 2008 financial crisis left the US economy one notch weaker with insipid growth and continued delays to the rate hike cycle. The current crisis may well do the same.

Banks are leveraged plays on GDP growth. Growth generally means higher rates and more transaction activity, which drives banks’ fee income streams. So the current uncertainties and risks of a weaker growth future aren’t good for bank stocks. Given Mr. Buffet thinks long term, him reducing banks is a reflection that he holds this concern now. And dumping WFC is an exit from a troubled bank in a troubled sector. You can’t say it lacks a certain logic.

The reason I think selling WFC may be a mistake is that while banks share the same subdued fundamental earnings outlook, WFC is a recovery story that may offer additional sources of upside against the sector-wide gearing to a macro recovery.

Capital is solid, costs are the problem

WFC is often described as When looking at a “troubled” bank, what do we mean? Is this a financial soundness issue or something more related to its P&L?

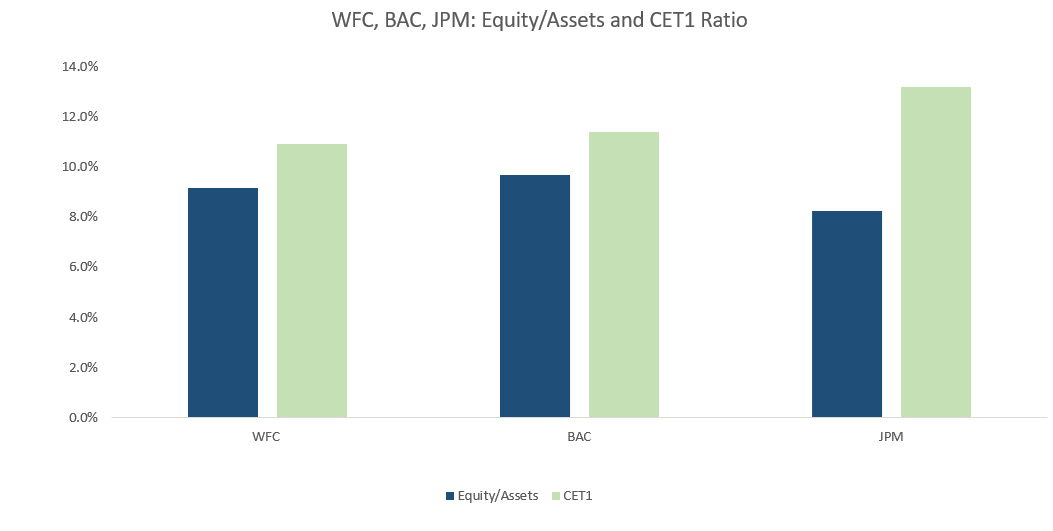

In terms of capital, WFC is absolutely fine with equity/assets and Common Equity Tier 1 Ratios comparable to Bank of America (NYSE:BAC) and JPMorgan (NYSE:JPM). JPM’s additional CET1 capital from lower equity/assets reflects a less lending intensive balance sheet. The point here is WFC’s troubled status does not include capital weakness.

Source: Company data

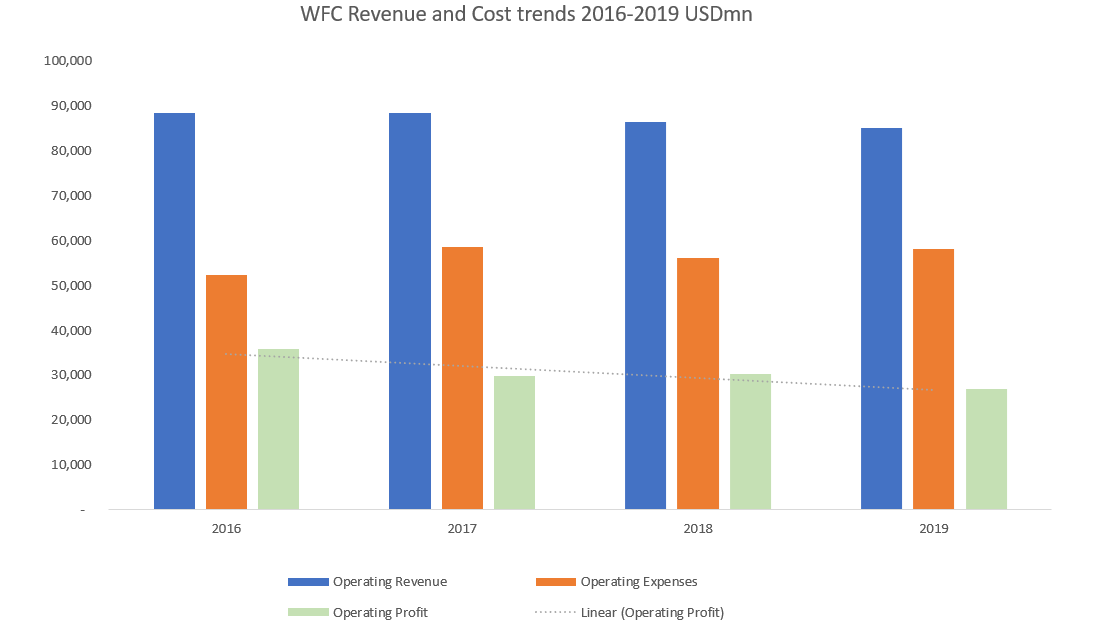

The problem is in the income statement, and it was evident before WFC underperformed its peers in the difficult 2020. From 2016 to 2019, WFC faced rising costs and pressured revenues.

Source: Company data

Let’s get two obvious things out of the way first. WFC does not have an extensive markets business, so BAC, and especially JPM, benefit from market volatility more than WFC. That’s OK. WFC is more exposed to an economic recovery when it comes.

The second thing is the asset cap. WFC can’t grow its total assets until the Fed is satisfied with its internal controls and management practices with regard to customer treatment. Problems in this area underlay WFC’s accounts scandal in 2016.

Some of the reader comments relating to the asset cap in my previous articles on WFC have not made sense. A number of people see it as a permanent feature. Investors should forget about this. Think of it in the following way: if the CEO of Wells Fargo failed to meet the Fed’s expectations, they would be removed by the board, and if that did not happen, activist investors would get involved. The Fed has no interest in such a major bank facing growth restrictions. The asset cap may well yet cause some frustration, but it is not a permanent feature.

Similar to the asset cap, some of WFC’s cost inflation has been due to one-off items such as regulatory costs and compensation with regard to the accounts from 2016. These costs will fall out going forward.

With this out of the way, what is the true problem?

Staff costs are key to the comeback

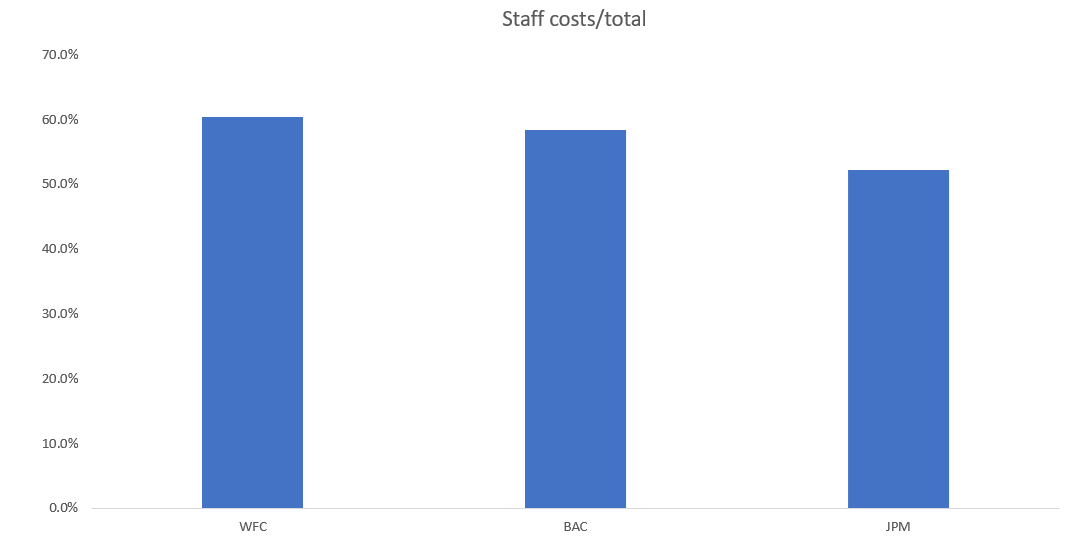

Since I last wrote about WFC, the bank has announced a resumption of executing on its extensive plans for headcount reduction. And looking at some of the metrics with staff efficiency in this bank, we can see that it is aiming at the right target.

WFC, for example, runs the highest level of staff expenses as a percentage of operating costs out of a sample of itself, JPM and BAC.

Source: Company Data

The data in these charts is based on 2019, which was a more normal year than 2020, and note that WFC carried additional costs last year related to the resolution of its accounts scandal. That means that staff costs/total costs are normally higher at WFC than its peers.

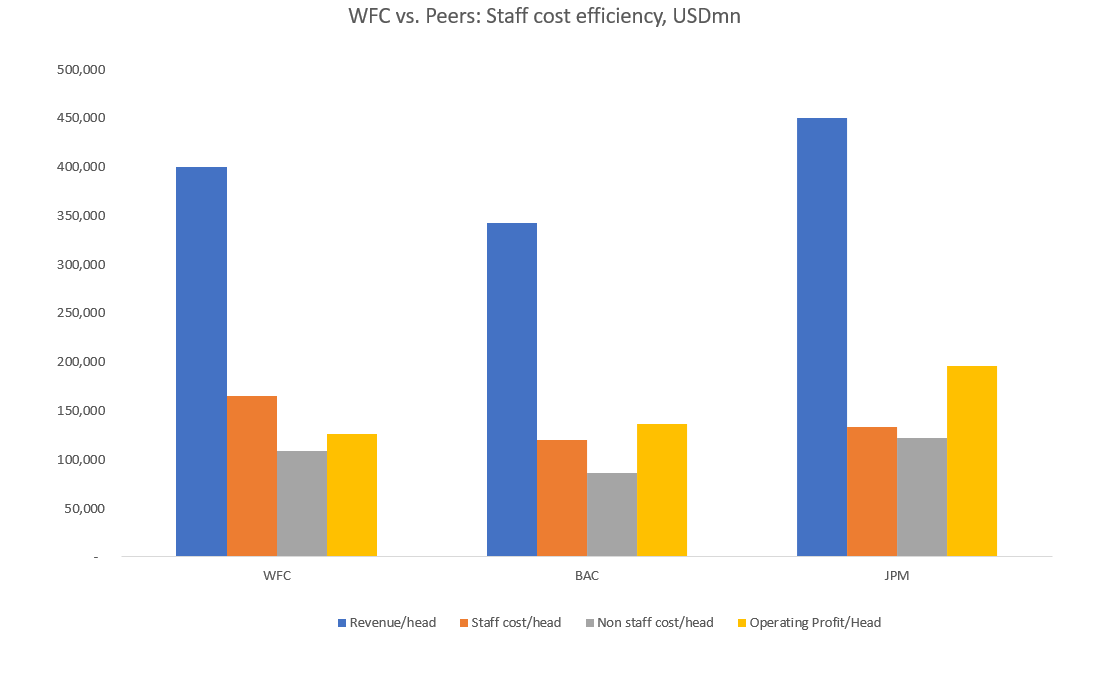

Now, revenue generation per head at WFC isn’t bad, lying between BAC and JPM. As you see below, it does less well in terms of both staff and non-staff costs per head (the orange and grey columns).

Source: Company Data

BAC does slightly better in terms of operating profit per head, while achieving markedly less revenue per head than WFC. The only area where JPM lags WFC is in its higher non-staff costs per head. But overall, it had the best staff efficiency of these banks.

Here’s a key chart in understanding this:

Source: Company Data

As you can see, although WFC has a large branch network in which there are opportunities for branch consolidation, its non-staff costs/revenue ratio is around the same level as JPM’s and BAC’s. This highlights just how far the problem at WFC are its staff costs.

BAC achieved much in its own improvement of operating cost/income leverage by not replacing retiring staff, and I noted the company’s comment on its last conference call that “a series” of employees had been told that their jobs would ultimately be cut. From my experience as a bank analyst, I expect incremental progress every quarter as this program gets going and will be asking the bank about eventual targets once we have some data to examine.

The problem in staff reduction is always whether a bank starts to impact its revenue levels by more than it expected. However, BAC’s success in the kind of changes WFC is embarking on suggests to me that what it is attempting is achievable.

Valuation

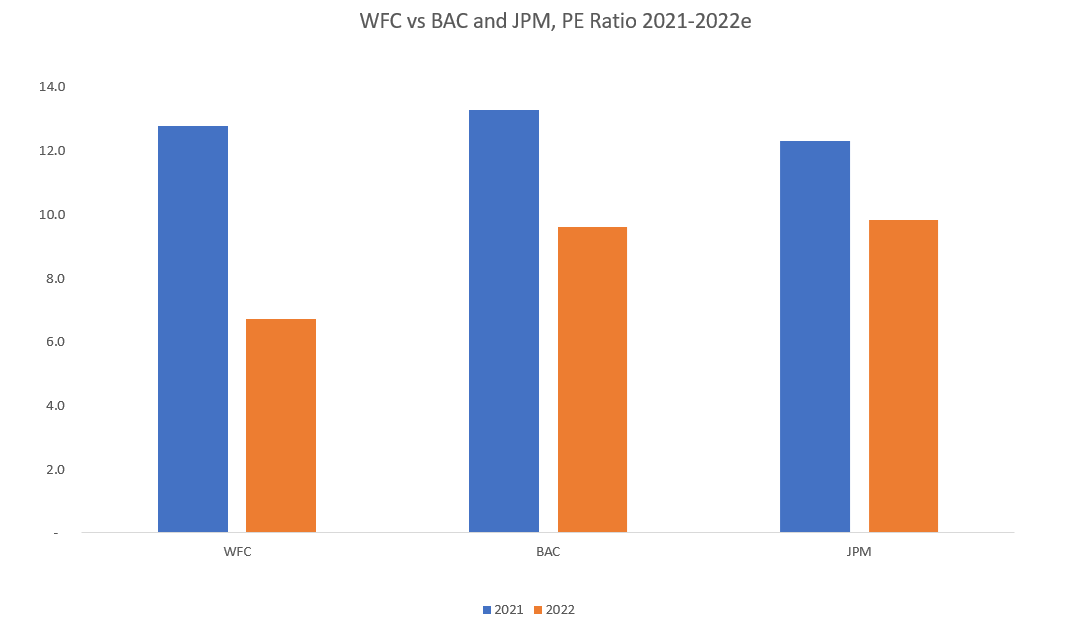

The market is not giving WFC a lot of credit for these cost plans. Its 2022 consensus PE ratio is far below those of its leading large bank peers.

While most analysts expect the asset cap to have been lifted by 2022, and for all banks to enjoy a somewhat stronger economy then, the cheap PE two years out shows the market is yet to be convinced that WFC will deliver stronger operating profits. Anyone looking at the numbers though will struggle not to include improvements in the forecasts, given management’s focus on the cost issue.

Conclusion

Berkshire may well be selling out of this bank as its management’s efforts bear down on the critical P&L of staff costs. Targets and incremental progress might make the disposal look poorly timed.

WFC has solid capital, good revenue/head and an announced cost reduction program to become more efficient. The bank has a lot of work to do, but in a macro environment that offers a slow comeback for the sector, additional sources of alpha from self-improvement are worthy of any fundamental investor’s attention.

If you found this article useful, please consider following me.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in WFC over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.