Let me preface this article by saying that I think you’ll have a hard time finding a company like Kesko (OTCPK:KKOYF, OTCPK:KKOYY). Its sector composition and business strategy are somewhat unique. The closest company I can think of is ICA (OTC:ICCGF), which I wrote about in my article entitled “ICA: Dividends From Half Of Sweden’s Grocery Market“.

In this article, I’ll show you why I consider these differences from similar companies to be part of the company’s strengths, and why I consider this to be a buy-and-hold-forever stock. Finland, together with Sweden and Norway, represents one of my primary areas of investment and capital allocation, and Kesko as a company represents almost 3.4% of my entire portfolio.

So, without further ado, let me show you why that is.

![]()

(Source: Wikimedia Commons)

{kind=link}

Kesko describes itself as a “Trading Sector Forerunner”. It operates in an interesting array of business segments, namely:

- Grocery trade

- Building/Technical trade

- Car trade

Much like Swedish ICA, Kesko was formed when four wholesaling companies merged during the early 20th century (1940). The driving force behind this merging was the need to purchase goods for retailers (who became shareholders) and start a larger degree of cooperation between retailers. Over the past 60 years, the group has gone through an incredible journey of serving small retailers around Finland, to the centralized organization that Kesko and the K-retailers are today. The ambition here was the improvement of an ever-evolving, customer-oriented and profitable operating model.

Over the past few years, the company entered the Swedish and Baltic markets. It took the company only a few years to become a market leader in the agricultural business in the Baltics ().

So, let’s take a more detailed look at these different sectors where Kesko is active.

Grocery/Food Trade

Kesko is the second-largest grocer in all of Finland in terms of market share and sales. The company’s role in the organization includes the purchasing of FMCG, selection management, logistics, and the overall development of chain concepts and the ever-growing store network (much like Swedish corp-similar ICA). Kesko manages three sizes of K-food chain stores.

The group has an overall market share of 36.0% (Source: ), and Finland holds about 1200 K-stores with 1.2 million daily customer visits. The stores are called K-Market, K-Citymarket, and K-Supermarket respectively.

Kesko is currently in the process of remodeling its stores, with 90% of the planned re-branding of K-stores and Neste K-Service Stations having been completed. The company primarily targets population growth centers as areas for opening new stores.

(Source: Kesko FY18 Report)

In terms of basic key metrics – sales and profit – the company is showing profitable development, with online sales growth over 70% annually (Source: Kesko FY18 Report). Kesko has also invested in K-Ruoka, a Finnish food media app, which already has over 600,000 users, which for a country with ~5 million inhabitants is quite impressive, representing 12% of the entire population.

(Source: Google Play)

The company has also started exporting food in collaboration with Chinese online store operator Alibaba (BABA).

The main competitors for Kesko in this segment are S-market (a cooperative, can’t be purchased on the stock market), which has a larger market share than Kesko, as well as Prisma, M-Chai, and Lidl (all smaller than Kesko).

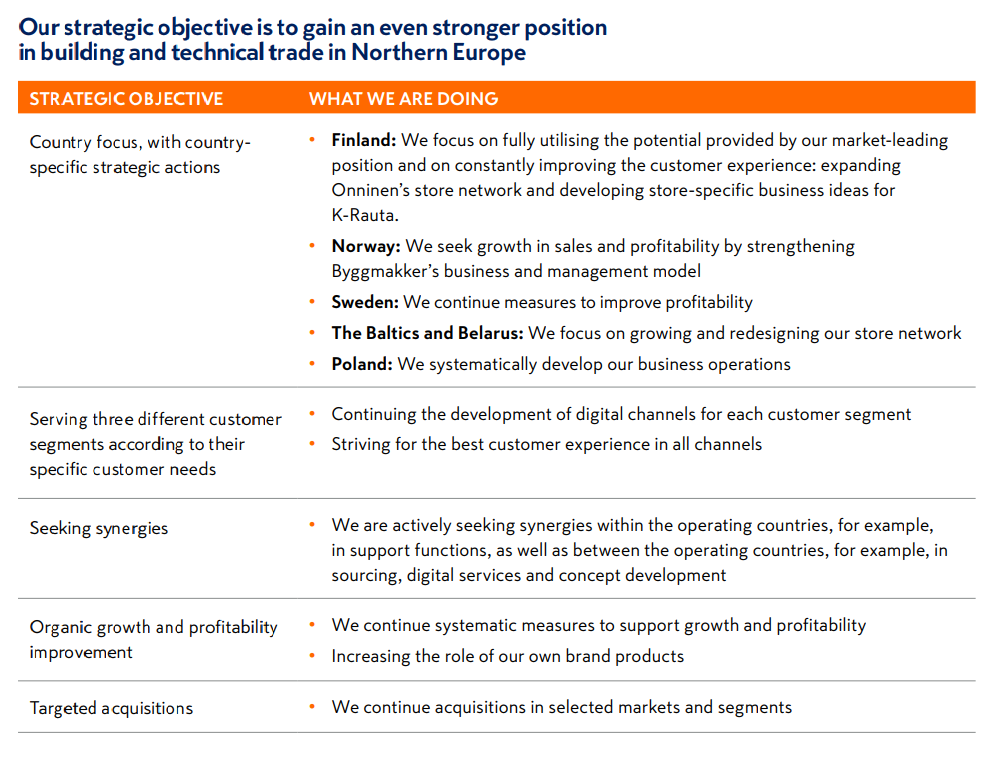

Building/Technical Trade

The segment consists of several stores, but the most significant of these is Finnish retailer Onninen and K-Rauta, which also exists in Sweden. The company also owns chains such as Intersport and Kookenkä, which are leading retail stores of sporting goods and shoes, respectively. The segment has representation, apart from these, in retail sales of clothing, home, leisure, home technology, entertainment, and furniture product lines.

The building trade provides retail services in building, renovation, and home improvement supplies across 8 countries. Apart from K-Rauta, chains K-maatalous, Byggmakker, Senukai, and OMA are included in the segment. Like K-grocery stores, the Finnish stores are owned by retail entrepreneurs.

(Source: Kesko FY18 Report)

Results during 2018 were somewhat mixed, with an increase in profits, while sales were down. The segment is still in the process of finding its edge in several markets. Divestments in Russia were completed during 2018, as well as Baltic machinery trade subsidiaries and agricultural machinery in Finland.

Investors can expect this segment to be characterized by acquisitions and further divestments in the coming years, where the company is seeking further synergies, acquisitions, and new possibilities all across Europe.

(Source: Kesko FY18 Report)

Car Trade/Technical Trade

Kesko’s car and machinery trade consist of the VV-Auto as well as Konekesko, with related subsidiaries. The company represents Volkswagen, Audi, and Seat. Through Konekesko, the company imports, markets, and provides service in all things recreational machinery, construction and material handling machinery/agricultural machinery, as well as trucks and buses. Konekesko operates in Finland and the Baltics.

Through its cooperation with VV-Auto and Konekesko, Kesko represents the leading brands in the area and is responsible for sales as well as after-sales services for these vehicles. The company also represents Porsche in Finland.

(Source: Kesko FY18 Report)

In addition, Kesko is also introducing its own cross-divisional mobility services. During 2018, the company began rental-sharing for passenger cars and vans, using already existing store networks in Kesko’s K-grocery store network to establish local stores as pick-up points for car sharing.

In terms of key metrics of sales and operating profit compared to 2017, we see similar results to the Building and technical trade segment, of increasing profits but lower sales due to macro concerns.

Kesko has also launched its own K-Charge network to start charging EV cars in Finland, then in connection with existing store networks.

Company Financials and Dividend

Kesko is an appealing combination of trades/sectors. The synergies that can be achieved by combining these different business segments are interesting – looking, for instance, at the EV sector, car sharing, and other ideas. The bottom line is that in Finland, a nation with 5 million inhabitants, Kesko represents a major player in the field of groceries, cars, machinery, building trade, and technical/home improvement trade. The company also works with Finnish and Baltics farmers, using existing networks to simply product entry into grocery stores and existing supply chains (such as to China, using Alibaba).

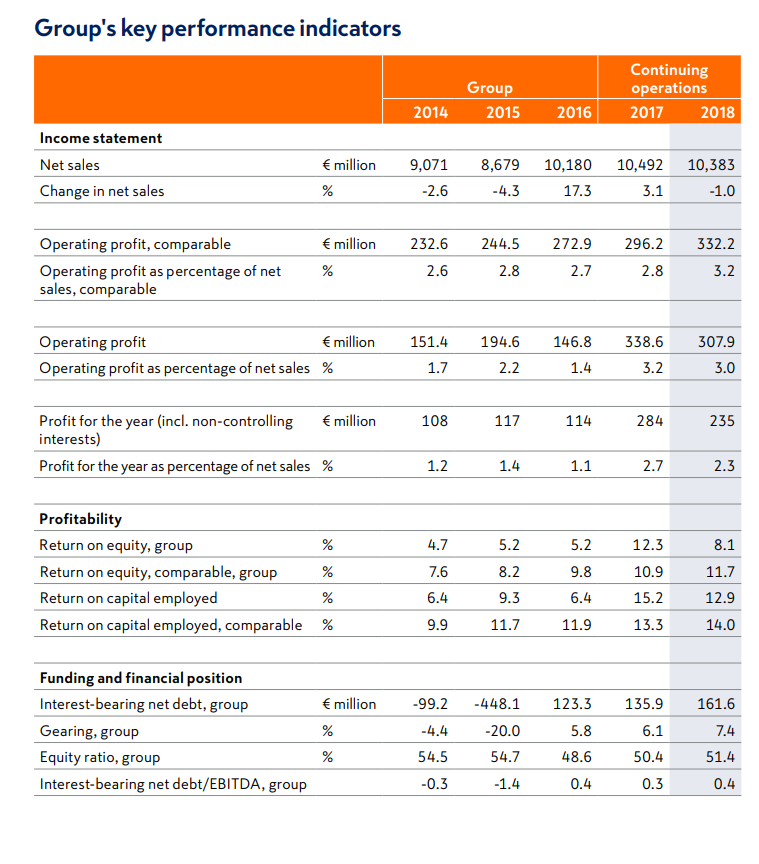

Let’s look at multiple-year comparisons for the company in terms of some key metrics.

(Source: Kesko FY18 Report)

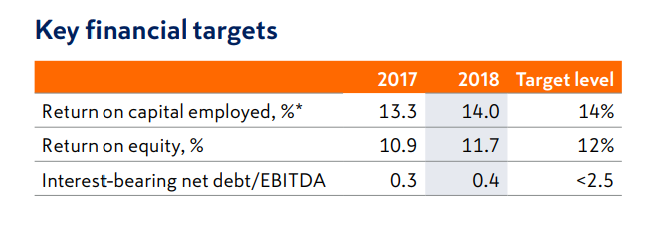

As we can see above, the picture of this company shows some very promising developments. The return metrics/profitability metrics for Kesko are all up over the period 2014-2018. While margins in Kesko are low, a mere 3% even at current improved metrics, the competition for this company within Finland can be characterized as “small”, and in that context, 3-4% margins are quite acceptable, as American grocery operators run under similar margin ranges.

It has managed to grow sales during this time as well, but I consider the increase in operating profit and margins a far more important/interesting metric, as it shows just how the company has managed to focus its earlier erratic operations into something far more streamlined.

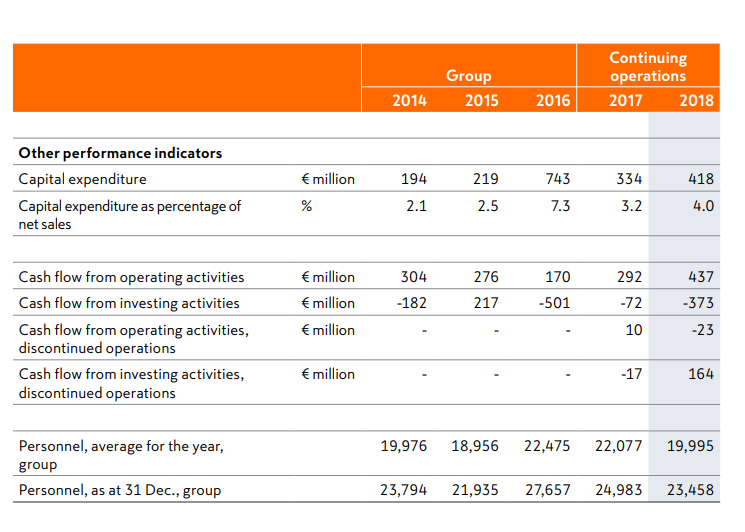

(Source: Kesko FY18 Report)

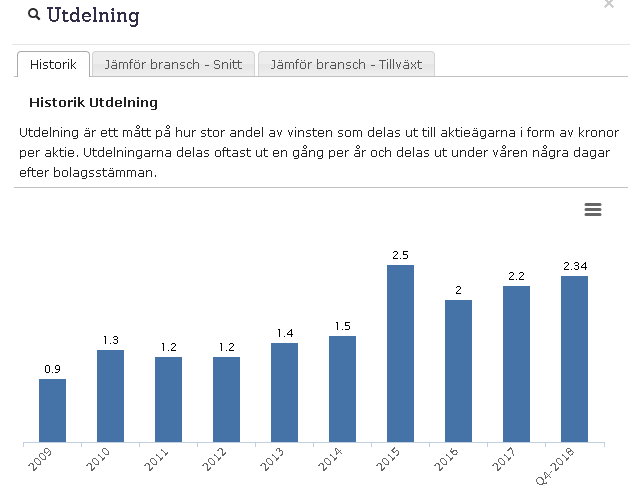

As we can see above, CapEx is still growing – the process of changing this company is not yet done. However, EPS during these years is up almost 50% (Source: Kesko FY18 Report), and the payout ratio has hovered at an appealing ~90-95% for most of these years. Some years, the dividend for Kesko has been at rates of the yield of almost ~8% (thanks mostly to bonus dividends), but most years the average share price keeps the dividend at about ~5-6%.

(Source: Börsdata)

The company is no stranger to paying bonus dividends either when it considers its financial situation to be good enough to do so.

Debt

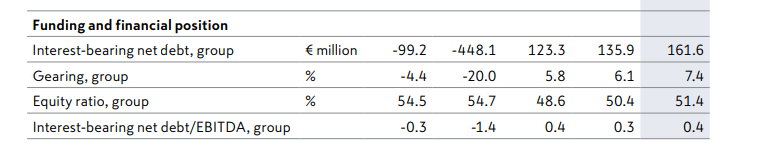

A quick word about Kesko’s debt situation. In one word – stellar.

(Source: Kesko FY18 Report)

Kesko follows the tradition of many other Finnish companies where debt/EBITDA ratios or total debt in relation to key metrics is extremely low compared to international peers. The company target lies somewhere below 2.5X, with current levels at 0.4X/EBITDA.

Wrapping up the basics

Kesko is a quite unique company combining a form of franchised retail of groceries, cars, and building/technical trade. These sectors are crucial for consumers of most any country, and in Finland, these all go under one roof: Kesko.

This appealing mix of company specifics and characteristics lead to two questions relevant before considering going further and investing in such a company.

Firstly, is the company doing well?

As we’ve seen going through recent financials, one could indeed argue that the company is doing quite well. Profit and efficiency for the past 4 years have only gone one direction – up – and Kesko says that this journey is as of yet far from over. The company is performing well in an essentially national oligopoly, where it represents 36% of the national grocery trade and sizeable bites of market share in all other areas as well.

As such, the company is doing rather well.

Secondly, what are the upcoming problems and challenges for Kesko and its various segments in the future?

For that, let’s move on to the second part of this article.

Kesko Challenges – not many, but worth looking into

This company’s market share precludes it from many otherwise-present challenges and negatives typically affecting a home market. The market share for K-stores and the breadth of their operation throughout even rural areas of Finland assures that entrants such as Lidl will be limited to a certain size of the market. At this time, Lidl has captured nearly 10% of the market (), making Kesko over 3 times as large in terms of market share and 4 times as large in terms of sales.

I believe the risks pertaining to the company are mainly two.

Firstly, we have M&A risks, combined with a high payout ratio

Kesko hasn’t yet earned the historical record to boast a reputation for executing successful M&As as a rule. The company has gone on record stating its desire to execute profitable M&As, and this during the same time when it is divesting other, current parts of its operation. As we know, M&As are inherently risky business, and the proposed synergies rarely work out exactly as the merging company/ies expect.

The risk isn’t inherently the M&A itself – at least not just that. It also includes the rather high payout ratio Kesko prides itself on. An over 90% dividend payout combined with potential risk and a failed M&A means one of two things – lower the dividend or extend the company’s debt.

While I mentioned that the company’s debt is at a stellar 0.4X in relation to EBITDA, this also needs to be put into context.

(Source: Kesko FY18 Report)

Kesko went from a -0.3X relation, a negative debt/EBITDA in 2014, to a positive 0.4X in 2018 – which is a difference of 0.7X, due to mainly rebranding, restructuring, and various M&As. Now, the company intends to continue acquiring other businesses; I believe this means it will be tapping credit facilities further in the future, meaning I don’t believe the company debt will stay at 0.4X. I believe we’ll be looking at 1.0X-1.5X within the next few years.

The risk of this needs to be considered prior to an investment.

Secondly, the company is active in some markets that could be considered volatile

With Swedish companies such as ICA, their Baltic operations are more of a footnote next to the revenues of their national/Scandinavian businesses. This isn’t the case for Finnish companies, and it’s not the case for Kesko. These firms have closer geographical proximity to the Baltics and eastern Europe, and both Kesko and other Finnish firms are more heavily entrenched in the Baltics.

Is this something inherently negative? Of course not – the Baltics are, in their own way, great nations with a lot of growth potential. However, there is no denying that Estonia, Latvia, and Lithuania suffer from higher rates of corruption and business risk going to the highest levels of government (Sources: and ).

I personally wouldn’t invest in a company situated/working strictly in the Baltics, though this is more due to my lack of knowledge about the companies in these states, but operating any sort of business in Eastern Europe is, in my view, subject to more volatile conditions and risk than operating it in western/northern European nations.

However, that’s more or less it.

One could argue that Kesko suffers from risks from competition in all of its segments, and that businesses such as home improvement, furniture, building/technical trade, and similar offerings are subject to competition from Amazon (AMZN). However, similar to Sweden, Amazon has not yet entered Finland, and I’ve yet to see a solution for how exactly Amazon is going to turn a profit while being situated in Sweden, considering the labor laws and logistical challenges it will face here, not to mention existing, established vendors that already have an online offering.

Now mind you, I’m not saying that I believe:

- Amazon will never come to Sweden/Scandinavia.

- Amazon will never be able to turn a profit in Scandinavia.

Because obviously, Amazon UK, FR, and DE already offer deliveries here. However, compared to Swedish retailers and offers, these products are often priced at similar and competitive levels to national retailers (with exceptions, of course). Amazon is also establishing some sort of presence here in Sweden (it’s hiring). However, any of the solutions currently working for Amazon in the USA/England probably won’t work in Sweden.

As for Germany, we need only look at the flak Amazon is taking for its hostile labor policies (Sources: , , , and ), with strikes breaking out during high-intensity periods such as Christmas.

Scandinavia, being of the Social-democratic welfare state model, has the most advanced and comprehensive worker-friendly labor laws in the entire world – and it’s had this for over 100 years. Amazon will not be able to act freely when opening offices and hiring people here, which will likely restrict the company’s margins and profitability in Scandinavia.

To name an example, the labor unions of Gothenburg harbor/Stevedores were able to, for the past 2-3 years, restrict harbor business/RoRo to such an extent (due to a wage conflict) that shipping companies no longer used/use the harbor, and several local companies went bankrupt.

The positives versus the negatives

It is my strong view that Kesko’s positives by far outweigh the potential risks of an investment in the company. It’s established market share in all areas, and active plans of growing further mean that the company’s potential losses in customer base and sales will be, at worst, limited. Its finances are in extremely good shape, with an almost non-existent debt, allowing Kesko to follow through with further acquisitions of other companies and also face any potential financial challenges.

The company has been spending increasing amounts of CapEx on current stores, rebrandings, and restructurings over the past few years – and this job (at least insofar as the grocery trade goes) is mostly finished at this point.

Because the company acts as somewhat as a franchise owner, the potential risk from a store closure/not going as well is also limited, as everything Kesko does goes through retail entrepreneurs who typically own more than one store. The expertise level in the store owners for Kesko is very high, and on average, much higher than say, that of ICA franchise owners.

Kesko dominates the market of several very popular car brands in the greater urban area of Finland – owning large shares of the market for VW’s cars, including Porsche, is a moat in itself (in my view).

In short, the risks to me in this company are mere footnotes next to the positives, and I highly encourage anyone interested in a ~5-7% yield from a company such as this to take a closer look.

But at what price?

Kesko’s valuation

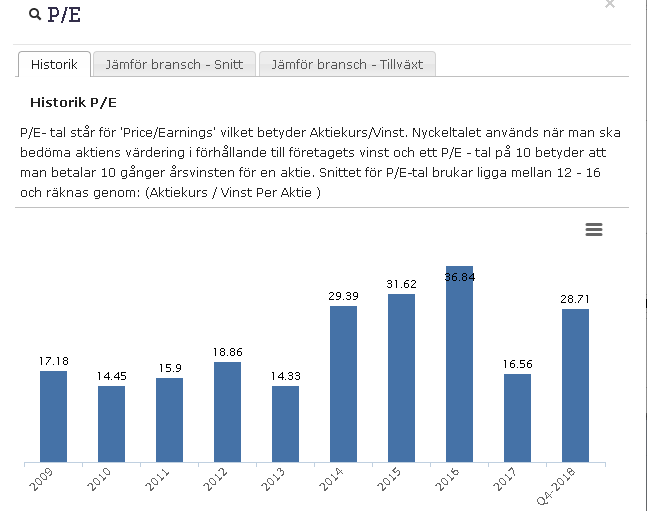

Kesko typically trades at a blended P/E ratio of 14-20. The current P/E ratio of 21.28 is, as such, historically and sector-specifically overvalued.

(Source: Börsdata)

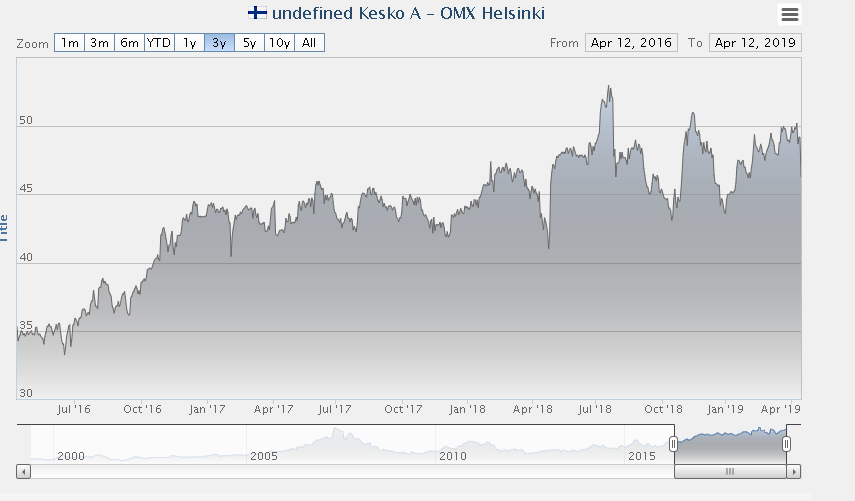

The historical trends for this company over the past few years are rather easily viewed. Catching this company at below a blended P/E of 20.0 during 2014-2018 has been rare. The maturity of its business and the fact that the company has been growing more and more effective have also meant that previous periods of extreme volatility, when the stock would jump between 20-40 EUR/share, are now much rarer.

What can be established is that at current valuations in terms of P/E as well as P/B and looking at company sales, Kesko is at the higher side of its typical valuation/price range.

The stock dropped nearly 6% during the past week due to a poor result with regard to the car trade (sales dropping ~21% in comparable terms). However, this development was in part due to the implementation of WLTP emission testing, resulting in car sales delays. All other areas for the periods of January-March 2019 showed growth, groceries up marginally and Building and technical trade up almost 5% ().

I’ve personally held the stock for almost 3 years, and bought it at a cost basis of 39.85 EUR (not including dividends). I don’t believe it’s realistic that we’ll see such a drop again, barring a recession.

Given Kesko’s current profitability, I consider a price below a blended P/E ratio of 18.0 to be undervalued given this company, indicating a 5.2%+ yield/share. I do not believe this to be a stock you should try to trade or swing-trade, but rather a strong B&H stock, as most of my Scandinavian grocers/trading companies are. Blended P/E ratios of ~20.0 or above are currently typical for the entire Scandinavian grocery market, as shares of Axfood (OTCPK:AXFOF) and ICA trade at similar or higher valuations. The entire space can currently be said to be overvalued.

(Source: Börsdata)

My preference would be purchasing Kesko at below ~42 EUR/share or a blended P/E of below ~18-19, representing at the very least a current “fair value”, if not a borderline undervaluation for a company of this caliber. At that level, I believe you would be locking money away in the grocery, technical, and car trade in an appealing, albeit niche, country (Finland is rather small in terms of population).

And I believe at a 5.5%+ yield, this warrants a second look.

My recommendation

I recommend you watch Kesko and prepare to initiate a buy at levels of 42 EUR/share or below, representing a blended P/E of ~18-19. Please observe that the stock price recommendation was calculated at the time of writing the article.

I will update this article or publish an updated thesis should things change, or/and in conjunction with future earnings updates.

Thank you kindly for reading.

Disclosure: I am/we are long KKOYF, KKOYY, ICCGF, AXFOF, AXFOY. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.