The monetary policy of several major central banks has captured the interest of financial market participants. For the first time in years, monetary policy is being coordinated on an international level with the aim of easing monetary conditions and stimulating the global economy. But in spite of the best efforts of bankers, one of the biggest problems facing the world economy is something they’re not prepared for.

In this report we’ll discuss a potentially major problem which is brewing – one that may require the direct intervention of the U.S. government. Here’s I’ll explain that continued dollar strength will put the economies of export-dependent nations at risk. And unless the dollar soon weakens, the next global crisis could originate not from the credit market but from the currency market.

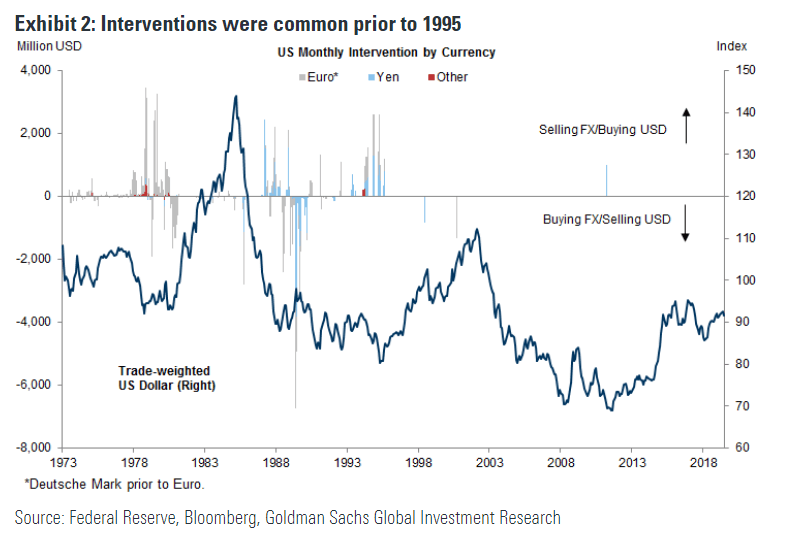

Earlier this summer, it was that the Trump administration was discussing the possibility of intervening in the currency market to weaken the dollar. The last time the U.S. intervened in the currency market was in 2011, which involved an attempt at weakening the Japanese yen following a destructive tsunami in March that year. This process involved the New York Federal Reserve and the Bank of Canada selling yen in exchange for their own domestic currencies, and also involved participation from the Bank of Japan. The intervention proved to be successful in weakening the yen on a short-term basis.

As a recent Goldman Sachs report explained, currency interventions were fairly common in the years before 1995. Since then, however, coordinated intervention among several countries has rarely been practiced due to an agreement to avoid competitive devaluations.

Source:

Source:

If the U.S. government were to intervene to weaken the dollar, it would involve join cooperation between the New York Fed and the Treasury Department’s $22 billion Exchange Stabilization Fund. And while the Fed engages in the actual buying and selling of currency, the U.S. Treasury traditionally makes the call as to whether or not to conduct an intervention.

President Trump is concerned that the dollar’s continued strength could undermine the U.S. economy and thereby weaken his chances at re-election next year. Trump also apparently the Fed’s “high” interest rates (relative to low U.S. Treasury yields) for the greenback’s strength. He also blamed the European Central Bank (ECB) for the dollar’s strength, recently tweeting:

They [the ECB] are trying, and succeeding, in depreciating the Euro against the VERY strong Dollar, hurting U.S. exports…. And the Fed sits, and sits, and sits. They get paid to borrow money, while we are paying interest!”

And while global investors are still averse to riskier assets like stocks, the U.S. dollar is still very attractive to many as a safe haven. The dollar has also recently benefited from the sharp decline in the British pound on Brexit-related concerns. The latest spike in the dollar’s value can be seen in the following graph of the Invesco DB U.S. Dollar Index Bullish Fund (UUP), which many investors use as a dollar index proxy. UUP hit a new multi-year high on Sept. 25 as worries about the global economy’s health continue to mount.

Source:

Source:

While a stronger dollar can be beneficial for U.S. consumers, its continued strength will eventually weaken the economies of countries which are reliant upon exports. Emerging nations which depend heavily dependent on agricultural and commodity-based exports are especially vulnerable to dollar strength. This partly accounts for the woes now being experienced by Argentina, a country whose federal debts are heavily in U.S. dollars. Indeed, the recent setbacks suffered both by Argentina’s peso currency and its equity market – as the Global X MSCI Argentina ETF (ARGT) illustrates – is reminiscent of the scare which Argentina and other emerging nations suffered in 1998 as a result of a strong dollar.

Source:

Source:

Currency strategist , who runs the Exante Data consulting firm, believes that a U.S. currency intervention is possible in the months ahead, especially if the quantitative easing policy by central bankers contributes to additional dollar strength. “That’s entirely new,” Nordvig told Bloomberg UK regarding a currency intervention. “That’s a new risk investors have not had to face for a long time.”

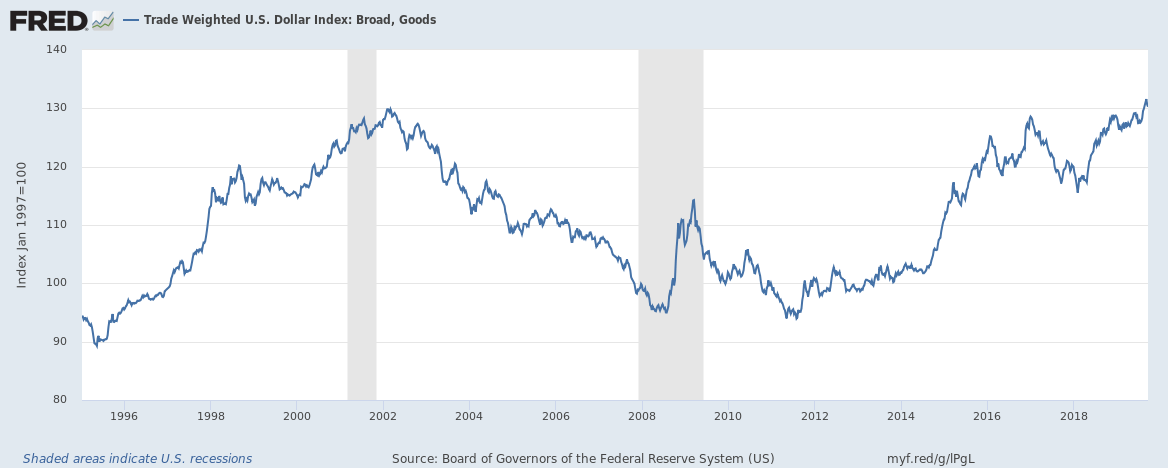

Although the U.S. equity market isn’t at risk from the strong dollar right now, the currency and equity markets of other nations clearly are. The last time the dollar was this strong was in the late 1990s-to-early-2000s, as shown in the Trade Weighted U.S. Dollar Index below. This period saw more than its fair share of currency crises (throughout Asia), economic depressions (Argentina), and heightened volatility in global equity markets. It would therefore be in the best interest of the U.S. government to consider a currency intervention if the dollar continues strengthening.

Source:

Source:

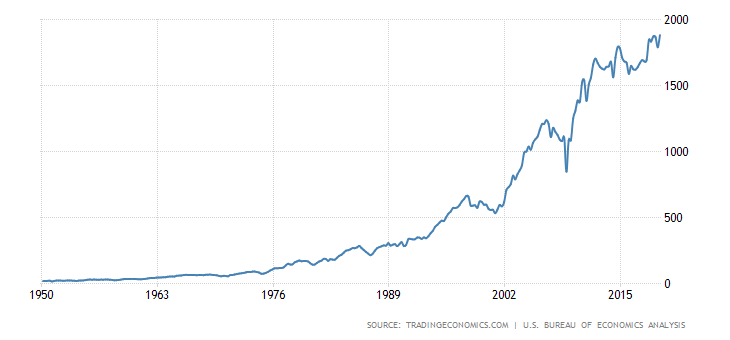

For domestic investors, however, it’s important to remember that a strong dollar can co-exist with a strong equity market. This was true in the late ‘90s when dollar strength actually helped contribute to the bull market in U.S. stocks, despite destabilizing foreign markets. It wasn’t until U.S. corporate profit growth began diminishing in the early 2000s that equities began to weaken. As the following chart shows, U.S. corporate profits are still rising at a steady pace and support a continued bullish outlook for domestic stocks.

Source:

Source:

If the dollar continues its ascent in the months ahead, investors should expect an aggressive response from both the Treasury and the Fed. This would be necessary to prevent another major outbreak of global market volatility and, quite possibly, a global economic slowdown. For now, though, the strong dollar isn’t hurting the U.S. economy or the stock market. A bullish intermediate-term (3-6 month) posture toward equities is therefore still warranted.

On a strategic note, I’m currently long the Invesco Dynamic Food & Beverage ETF (PBJ). As discussed in a recent report, my research indicates that food retail stocks are among the top relative strength and earnings growth leaders of the broad market. I’m using a level slightly below the 34.20 level as a stop-loss for this trading position.

Disclosure: I am/we are long PBJ. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.