Baidu stock is trading about 25% lower since it released its Q1’19 results on 16 May (and a whopping 60% below its all-time high!), largely due to the company surprisingly posting its first loss in over 13 years. Investors have punished the Tech giant, with the company now trading at a very inexpensive, dwarf-sized 20x 12-month forward P/E (Source: Bloomberg).

In this article, I detail Baidu’s dominance in China’s search market, as well as give some perspective on the reasons why investor concerns may be inflated. From a technical perspective, Baidu stock is flashing strong over-sold signals, and I believe this is a very rare opportunity to pick up the stock for potential out-sized gains.

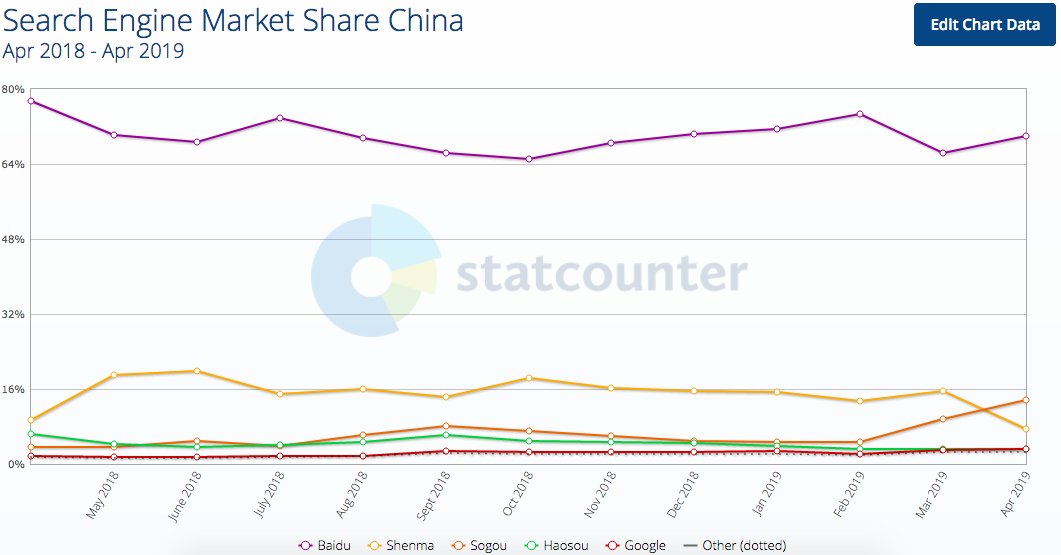

Baidu’s Leadership in China’s Search Market

Baidu (BIDU) is known as the “Google of China”, with an estimated 70% market share in China’s search engine space, according to Statcounter. Their “competition” is largely scattered across 3-4 other small players, all controlling less than 15% market share each.

Source: StatcounterThis competition includes Google (GOOGL), which is caught between a rock and a hard place. After pulling out of China’s search market in 2010 after co-founder Sergey Brin protested against the Chinese government’s “totalitarian policies”, Google has attempted to re-enter the lucrative market via Dragonfly, a censored search product for China. This has not gone down well with human rights advocates and lawmakers.

Source: StatcounterThis competition includes Google (GOOGL), which is caught between a rock and a hard place. After pulling out of China’s search market in 2010 after co-founder Sergey Brin protested against the Chinese government’s “totalitarian policies”, Google has attempted to re-enter the lucrative market via Dragonfly, a censored search product for China. This has not gone down well with human rights advocates and lawmakers.

To add fuel to fire, the Trump administration has banned US companies from doing business with Huawei. Google has joined a host of companies such as Broadcom (AVGO), Qualcomm (QCOM), Intel (INTC) and Microsoft (MSFT) to cut ties with Huawei, by announcing it would cease providing support to Huawei phones, and will take away their access to the Google Play Store app marketplace, as well as applications such as Gmail and YouTube.

This makes it extremely difficult for Google to re-enter China’s lucrative search market. In essence, a protracted trade war between US and China will help Baidu fend off competition from the world’s number one Search company in its domestic market. Talk about silver linings.

Breakdown of Baidu’s FY18 Revenues Source: Company Annual Report FY2018Baidu’s dominance in China’s search market is expected to continue, and this has thus far given rise to a CAGR of about 12% in the company’s “Online Marketing Services” revenue segment from FY14 to FY18.

Source: Company Annual Report FY2018Baidu’s dominance in China’s search market is expected to continue, and this has thus far given rise to a CAGR of about 12% in the company’s “Online Marketing Services” revenue segment from FY14 to FY18.

Baidu’s Expansion into Video Streaming – Think Netflix of China

Aside from its core search business, Baidu owns a c. 58% stake in iQIYI (IQ), known as the “Netflix of China”. In the recently released Q1’19 results, iQIYI announced it has 96.8 million subscribers. This compares with c. 148 million subscribers Netflix (NFLX) has currently.

Baidu announced its first loss in more than 13 years in its Q1’19 results. The main culprit was the company’s cost of revenues surging 50%, largely due to aggressive investment in new content for iQIYI.

While investors have punished the stock, I remain of the view that such investment into iIQYI is necessary for iQIYI to cement its leadership position in the very lucrative online entertainment market in China. iQIYI continues to enjoy a lead over its closest contender, Tencent Video, which has c. 82 million users as of February 2019. The online entertainment market in China is huge, and is expected to grow at a CAGR of c. 30% from 2012 to 2022. In 2022, the market is expected to be worth c. USD 100 billion (USDCNY = 6.90).

Looking at Netflix’s case, the company only managed to turn a profit for 5 of the years between 2002 to 2018. In 2018 (the company’s most profitable year), Netflix’s net income margin was a measly c. 7.5%. As such, I would advocate investors to remain patient over iQIYI (and Baidu). Investment into the online entertainment market is necessary to win over subscribers, and iQIYI has found joy in growing its subscriber base so far. The profit will come later (the company expects to turn a profit only in 2020-2021), and the online entertainment market size in China definitely justifies Baidu / iQIYI’s investments.

Looking at Netflix’s case, the company only managed to turn a profit for 5 of the years between 2002 to 2018. In 2018 (the company’s most profitable year), Netflix’s net income margin was a measly c. 7.5%. As such, I would advocate investors to remain patient over iQIYI (and Baidu). Investment into the online entertainment market is necessary to win over subscribers, and iQIYI has found joy in growing its subscriber base so far. The profit will come later (the company expects to turn a profit only in 2020-2021), and the online entertainment market size in China definitely justifies Baidu / iQIYI’s investments.

Baidu’s Future-oriented Research Arms – Think Google

Baidu is not simply a search company. It has invested in various technological fields which are likely to pay dividends in the future. Baidu Research, which has offices in Silicon Valley, Seattle, and Beijing, “brings together top talents from around the world to focus on future-looking fundamental research in artificial intelligence“.

Its research areas are multitudinous – including data science and mining, robotics and autonomous driving, machine learning and deep learning, and quantum computing.

Does this not resemble Google’s research and development arm, Google AI, which has similarly invested in a vast number of technological fields for the future?

Not many technological companies have the scale, capabilities, infrastructure and talent to do what Google does. While Baidu may not be on the same stage as Google, its investments in technological research and development will ensure the company will remain at the forefront of some of the world’s most cutting-edge technologies.

Technical Perspective – Stock is Heavily Oversold

First, Baidu is trading at a whopping 60% discount versus its all-time high. Next, some of my technical indicators are showing that the stock is massively oversold:

- The magnitude of BIDU’s recent sell-off is more than 3 standard deviations (based on price action of previous 20 weeks)

- Short interest levels in BIDU have risen to levels only matched once in the past 5 years (in 2016). A short squeeze may see an outsized rally in BIDU stock

- BIDU’s 10-day volatility has risen to levels only matched once in the past 5 years (in 2018)

- BIDU is trading at levels last seen in 2015. Previously during that week, BIDU staged a rebound to close above $152, indicating there might be strong support around current levels

Source: Tradingview.comPutting together everything, Baidu may have experienced a bad quarter, but this can be explained by the company’s aggressive investment in developing video content for iQIYI. Taking into account the online entertainment market size in China, I believe this investment is warranted, and it is necessary for iQIYI to continue to cement its leadership position in the market.

Source: Tradingview.comPutting together everything, Baidu may have experienced a bad quarter, but this can be explained by the company’s aggressive investment in developing video content for iQIYI. Taking into account the online entertainment market size in China, I believe this investment is warranted, and it is necessary for iQIYI to continue to cement its leadership position in the market.

Going forward, Baidu should continue to reap dividends from its strong leadership position in its core search engine business, with the US-China trade war essentially curtailing Google’s ventures into this market. Competition remains scattered and is unlikely to threaten Baidu in the near future.

Baidu’s dominance in China’s search market, coupled with its future arms of growth (video streaming, machine learning, autonomous driving, etc.) should see the stock trading much higher than its 20x forward P/E currently.

Lastly, Baidu stock looks massively oversold from a technical perspective. The high amount of short interest in the stock in particularly, makes the stock vulnerable to a short squeeze, which could see it enjoy an outsized rally in the near future.

Is this the bottom for BIDU? It is difficult to say. The stock could continue to trade lower, but I strongly believe the risk-reward is heavily tilted to the upside for investors.

Disclosure: I am/we are long BIDU. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.