Summary

The eurozone is facing a high degree of financial strain as a result of the COVID-19 crisis.

While the €750 billion ECB stimulus package has temporarily averted a spike in bond yields, higher borrowing costs for peripheral economies remain a possibility.

The EUR/USD could end up trading below parity within a year.

The EUR/USD has seen a significant increase in volatility throughout the COVID-19 crisis.

Source: investing.com

Questions regarding the future of the eurozone – while present – took somewhat of a back seat before this crisis.

However, this issue has now come to the forefront once again. With EU leaders having failed to reach a regarding the issue of “coronabonds” to help weaker economies such as Spain and Italy weather the crisis, questions are now being raised as to whether the eurozone is the ideal vehicle for peripheral economies to weather this crisis.

In addition, traditionally open borders across the Schengen area have brought into question whether such a policy is sustainable going forward – given that a lack of control over borders has facilitated the rapid growth of COVID-19 across Europe.

Since 2015, there were concerns that the EUR/USD could eventually reach parity. While the euro has maintained strength up till now, this may well be the crisis that pushes the currency over the edge.

Of course, with the having been lowered to near zero, the greenback will inevitably see periods of weakness during this crisis.

With that being said, currency markets in general appear to be highly volatile right now. For instance, the Japanese yen – traditionally a safe haven currency – has also seen large fluctuations against the USD for the month of March:

Source: investing.com

The currency market is likely to remain highly volatile as the world economy continues to “lockdown” given the unprecedented nature of this crisis. As such, the EUR/USD is likely to continue to oscillate strongly without any clear trend in the near-term.

However, I take the view that the COVID-19 crisis will mark a significant turning point for what some would call a long overdue discussion regarding the future of the Eurozone. While questions have always remained regarding the structure of the EU along with growing concerns including Italian debt and the possibility of Italy leaving the eurozone, the COVID-19 crisis only seeks to accelerate the debate on these issues.

As such, I cannot foresee that the EUR/USD will remain above parity over the next year given the current circumstances.

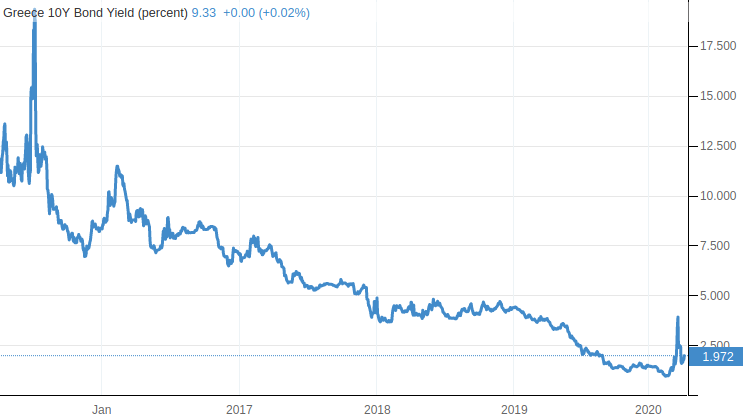

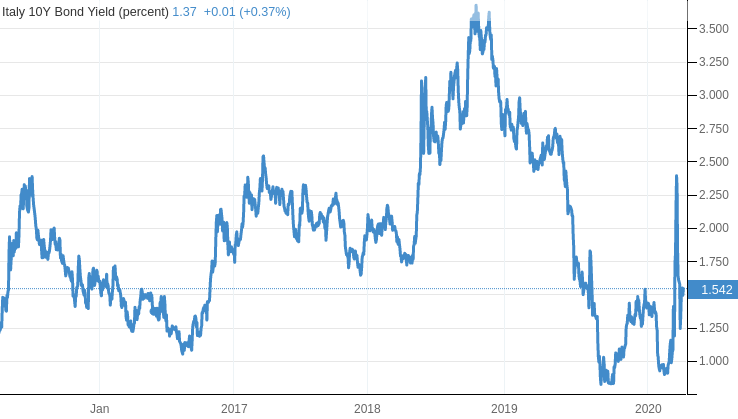

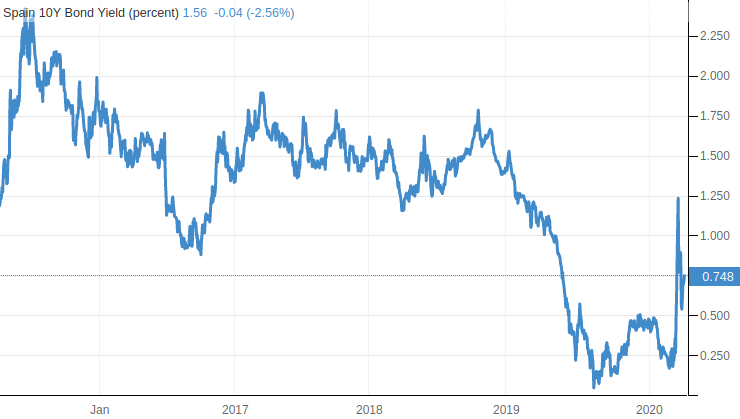

That said, the actions of the are helping to mitigate the crisis somewhat. With the ECB having unleashed a €750 billion stimulus package as part of its emergency response, we can see that 10-year bond yields for Greece, Italy, and Spain remain significantly below the 5-year average trend. In the absence of such stimulus, the cost of borrowing for these countries would have been much higher.

Greece 10-year bond yield

Source: tradingeconomics.com

Italy 10-year bond yield

Source: tradingeconomics.com

Spain 10-year bond yield

Source: tradingeconomics.com

With this being said, much hinges on how much longer the crisis is set to continue. There is every possibility that the cost of dealing with the COVID-19 crisis continues to rise to unsustainable levels and bond yields could eventually rise further. Should this happen, then I see this as being a significant indicator of euro weakness ahead.

The EUR/USD is quite volatile at this point in time and I would not trade the currency under these circumstances. However, the pressures of the COVID-19 crisis on the eurozone cannot be understated and the euro could well see a weakening below parity against the USD in the year ahead. This would be unprecedented – but so is this crisis.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.