The end of last week saw the release of results from multiple studies of Gilead Sciences (GILD) remdesivir, but the stock finds itself more or less in the same spot as it was before the data. This article takes a look at why that might be and what could trigger a change in the share price.

Figure 1: Past month of GILD trading.

Remdesivir data no slam dunk

The first reason GILD might not have experienced a sustained rally relates to the data seen with remdesivir itself in COVID-19.

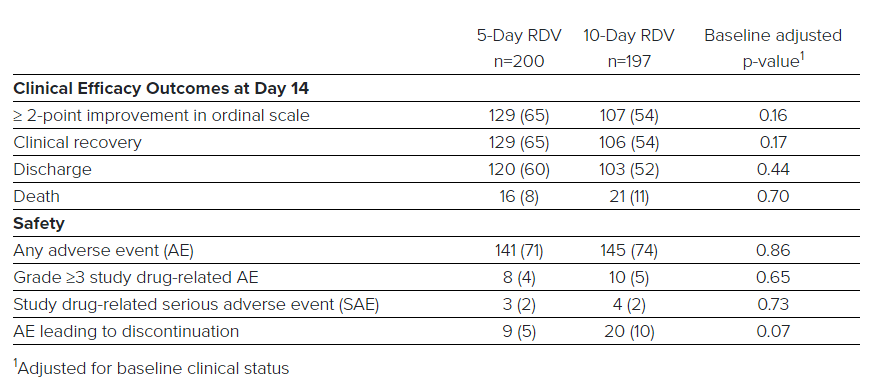

GILD’s SIMPLE study comparing five days of remdesivir to 10 days in severe COVID-19 produced an uninterpretable result. Five days of therapy was numerically more likely than 10 days to produce ≥ 2 points of clinical improvement, produced greater rates of clinical recovery and discharge, and also lower rates of mortality. Thankfully, those differences were only trends, there was no statistical significance.

Table 1: Key efficacy and safety data from GILD’s SIMPLE Phase 3 study. Source: April 29 .

With results from the SIMPLE study, we are left asking if five and 10 days of remdesivir are equally effective, or equally ineffective. How are we supposed that result? The fact that the benefit trended towards five days of therapy vs. 10 days of therapy doesn’t help matters.

Fortunately, we also have data from the National Institute of Allergy and Infectious Diseases (NIAID) study which were much more convincing. Preliminary results from The Adaptive COVID-19 Treatment Trial the time to recovery was 31% in COVID-19 patients treated with remdesivir compared to those treated with placebo (p<0.001). There was no mortality benefit (8% remdesivir vs 11.6% placebo, p=0.059) but a near miss.

One of the issues with this trial is the fact that the primary endpoint was switched mid-study. The NIAID has for the endpoint change but questions still remain as the study is not published yet.

Figure 2: Changes in the primary endpoint that occurred on April 16 (right) compared to a protocol available on April 2 (left). Source: Clinicaltrials.gov site.

Considering the totality of the data across trials of remdesivir, I am still struggling to work out if the drug works or not, but others are convinced and still others are keen to suggest remdesivir is .

I believe slight uncertainty over the validity of the result may be a factor in GILD’s share price failing to break above recent highs. That being said, I didn’t think the market would be expecting a slam dunk result with remdesivir so concerns may be coming from elsewhere.

Is GILD going to make any money off this?

The second factor that may be holding GILD down relates to the profitability of remdesivir. It makes sense that there are concerns over this, the development and scale-up of remdesivir has already cost GILD.

Now, turning to our expenses, non-GAAP R&D expense was $1 billion for the quarter, up 8% compared to the same period last year, primarily due to the ramp up of Remdesivir, including manufacturing scale up and clinical trial costs.

Andrew Dickinson, CFO at GILD, Q1’20 earnings call.

The 140K courses of remdesivir that GILD has donated could last just months or less, and the company intends to produce 1M courses by year-end, meaning the potential to start charging for the medicine exists. The FDA has provided Emergency Use Authorization which means use will now expand rapidly. The problem is we might be waiting a while for clarity as GILD was unwilling to provide clarity on what the business model will look like with remdesivir in the future.

Given the continued uncertainty in the trajectory of the pandemic and in Remdesivir clinical data, it’s premature to define what the right post donation business model is to create a sustainable long term supply for global needs. In the context of strong underlying business and Q1 results, we will continue to monitor the situation and expect to provide additional insights and outlook on our Q2 earnings call.

Andrew Dickinson, CFO at GILD, Q1’20 earnings call. Emphasis mine.

Analysts tried to get additional information out of the company on potential revenues and the business model for remdesivir, but were unsuccessful. That lack of clarity is exactly what the market doesn’t like.

Accessing different patient populations may be challenging

GILD’s remdesivir is administered as an IV infusion. The ability to provide the treatment to non-hospitalised patients then would require hospitalisation or the patient attending an infusion centre. If you’ve got COVID-19, we’d probably rather that you don’t travel back and forth to an infusion centre for 10 days (or five days). An infusion could also be possible at aged care facilities and other similar facilities for those who require round-the-clock care. We first need some evidence that remdesivir is effective in non-hospitalized patients or in mild/moderate COVID-19. These are the sort of patients you might be able to treat outside of a hospital, or treat at first in the hospital and then discharge earlier than otherwise when improvement is seen. Overall if remdesivir could be formulated as a pill, that would be a big advantage. The problem is, Daniel O’Day has confirmed that an oral formulation isn’t in play.

It’s not, this particular medicine, because it’s heavily first half metabolized in the liver, is not really appropriate as an oral formulation. We’ve known that for years, probably a decade. But we are looking into things like subcutaneous formulations and potentially inhaled formulations. And although, it’s too premature to give you timelines on that, rest assured that we’ve been actively working on those.

Daniel O’Day, CEO at GILD, Q1’20 earnings call. Emphasis mine.

Both subcutaneous and inhaled formulations of remdesivir are going to have lower bioavailability and more variable bioavailability, but would have the advantage of potential administration via a patient. It sounds like GILD is hard at work, but there isn’t any clarity on that yet either, bringing into question how many patients will be treated with remdesivir, and how it might compete with other oral therapies, should they produce compelling data in COVID-19.

Conclusions

The good news comes from GILD’s results for Q1’20, the company has experienced little headwinds due to COVID-19, product sales of $5.47B were up 5% from the same quarter in 2019 ($5.2B). The problem is that this increase appears to be largely ($200M) due to customers stocking up on prescriptions, and so revenue may soften in future quarters. EPS of $1.22 was down 21% from Q1’19, although non-GAAP EPS of $1.68 (0.6%) was almost flat.

The bad news comes from uncertainty on remdesivir, and that has stopped GILD rallying further. Firstly, a lack of consensus on the remdesivir results. Are these results meaningful without a mortality benefit and do they really show that remdesivir works? Secondly, a lack of clarity on the profitability of remdesivir. GILD could spend up to $1B in 2020 on the drug, but what revenues will it bring in? Thirdly, GILD’s ability to tap additional COVID-19 markets is still in question. Remdesivir being an infusion instead of a pill puts it at a disadvantage to other potential COVID-19 therapies (should they succeed) in select patients.

Figure 3: Select studies of remdesivir, note the moderate COVID-19 study (4th row). Source: GILD Q1’20 earnings call presentation.

I can’t see GILD exiting the current trading range (high $70s to low $80s) until we get clarity on the potential revenues from remdesivir or at least a result in moderate COVID-19. Data from that study will come in late May. Another potential catalyst would be a switch from emergency use to full approval. If the NIAID study is sufficient for full approval as Daniel O’Day speculated on the conference call, then that might only be weeks away as well.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.